Answer: c) Latency between her VPN client removing encryption and making it available to the video-conferencing client is causing poor performance.

Explanation:

A Virtual Private Network (VPN) is used to protect the identity of people online as it encrypts a person's data and uses different servers to allow them browse the web and with a different IP address from the user's original IP address that way it appears as though the user is somewhere else in the world than they actually are.

In doing this however, VPNs might give slow speeds due to the latency that develops as the VPN encrypts and decrypts data for use. In this case, the VPN latency in decrypting the video call for Consuela to see it is slowing down the speed of the Video conferencing client.

Answer:

c. cease production immediately, because it is incurring a loss.

Explanation:

When a business engages in production it looks to make profit. That is for the production price to be higher than cost incurred in producing the good.

However when the price is lower than the average variable cost as is indicated in the scenario then the firm needs to shut down production in the short term.

Factors that will adversely affect a firm in the short term are price, average total cost, and average variable cost.

Once price is less than average total cost or average variable cost it is better to stop production.

As they are incurring an economic loss

Answer:

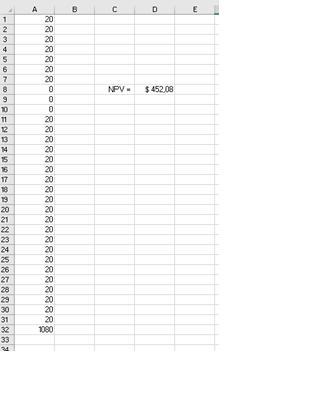

I used an excel spreadsheet to calculate the bond's value (see attached image). the bond's intrinsic value using a 11% discount rate is $452.08

Explanation:

Answer:

A prejudiced discriminator

Explanation:

A prejudiced discriminator is someone who actively and openly discriminate against others based on their religion, race, disability, gender, age, and among others. They do these by actively committing hate crimes and make disparaging comments about others. Prejudiced discrimination can also be committed through their action like refusing to employ some set of people because of their religion, race, disability, gender, age, and among others.

There are also prejudiced non-discriminators who are different from prejudiced discriminators, because prejudiced non-discriminators do not act on act racist that they harbor like prejudiced discriminators who harbor it and at the same act on it.

I wish you the best.

Answer:

Blue Spruce Corp.

Statement of Comprehensive Income

Income before income taxes $436,000

Less: Income Tax <u>$139,520</u>

($436,000 * 32%)

Net Income $296,480

Other comprehensive income (loss):

Unrealized gain on available-for-sale <u>$58,140</u>

securities, net of tax ($85500*68%)

Total Comprehensive Income <u>$354,620</u>