Answer:

$149,600

Explanation:

Variable cost per unit = 36+57+3+5 =

Variable cost per unit = $101

Contribution margin per unit = 145 - 101

Contribution margin per unit = $44 per unit

Total contribution margin = 3,400 * $44

Total contribution margin = $149,600

Answer: A merger involves one company purchasing the assets of another company with cash, whereas an acquisition involves a company acquiring another company by buying all of the shares of its common stock.

Answer:

see below

Explanation:

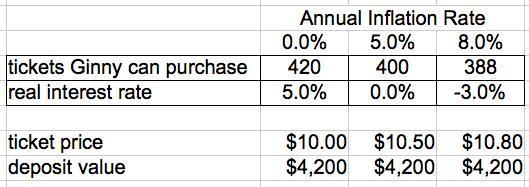

The balance in Lucia's account is 1.05 times the original deposit, reflecting addition of 5% interest for the year.

The ticket price is the original price multiplied by (1 + inflation rate). The number of tickets that Lucia can purchase is the account balance divided by the ticket price. The quotient is rounded down to the nearest integer.

The "real interest rate" is the percentage change from the original number of tickets that could be purchased.

Answer(1)

<em>b. interest rate at which banks can borrow reserves from the Federal Reserve</em>

Explanation:

The discount rate is known in America as the rate of interest which a central bank charges on its loans and advances to a commercial bank. This loans and advances are from the federal reserve.

Answer (2)

<em>a. more reserves, causing an increase in lending and the money supply</em>

Explanation:

Excess lending from the national reserve due to a lowered discount rate will lead to a reserve supply excess into commercial banks throughout the economy and expands the money supply .

Answer:

$206,000

Explanation:

Beginning inventory 10,000*9.2 $92,000

Purchases during the month (9000*8+ 6000*7) $114,000

Cost of Goods available for sale $206,000