Answer:

Monthly bank statements should be sent to and reconciled by the same employees who authorize payments and write checks

Explanation:

Answer:

The correct option is (d)

Explanation:

Products have a cycle starting from introduction, growth, maturity and decline. This is called product life cycle. Considerable investment is required at introduction stage. Once the product is profitable, it enters growth stage and at maturity, it is at the most profitable stage. A product reaches decline stage as competitors step in and better products are made available in the market.

By adding features to its models, BMW is trying to lengthen its product life cycle so as to avoid the product's entry to decline stage soon.

Managers need to understand the possible dangers associated with a job to ensure work is being done safely. Understanding job requirements is critical to making intelligent hiring decisions.

<h3>What is

Managers?</h3>

A manager is a qualified someone who leads an organization and oversees a group of workers. Managers frequently oversee a certain department within their organization. There are many different kinds of managers, but they typically have responsibilities including making decisions and conducting performance reviews.

A manager is responsible for tasks like staffing, directing, controlling, and planning. All of these tasks are crucial for successfully managing an organization and accomplishing corporate goals. Setting goals and developing techniques for synchronizing activities both involve planning.

A business manager is responsible for managing and directing the activities and personnel of a company. They carry out a variety of duties, such as implementing business strategy, assessing business performance, and managing staff, to ensure the productivity and efficiency of the company.

to know more follow Managers the link:

brainly.com/question/24553900

#SPJ4

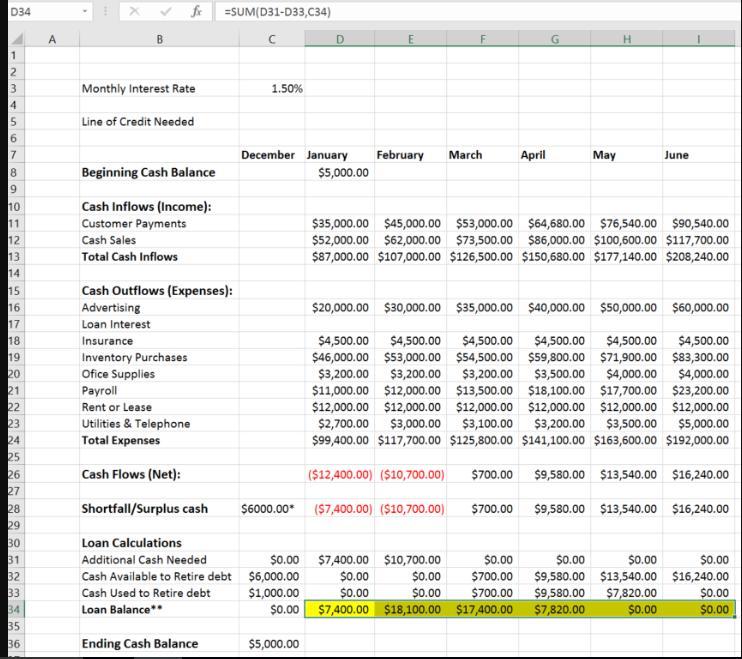

Answer:

The closing balance from the excel sheet is $5,000.00

Explanation:

Solution

Given that:

The loan balance required l for each month can be computed as follows:

The loan balance = additional cash needed – cash used to retire debt + loan balance from previous month

Now

By applying the excel formula to perform this task is stated as follows:

D34 = SUM(D31-D33,C34)

The same formula is used to get the values for E34 to I34.

Kindly find an attached copy of the updated excel sheet after applying above formula which is a part of the solution is as follows:

Answer: A, B, and C. ALL OF THE ABOVE!

Explanation:

They're all the correct answer.