Answer:

B. Purchase Price of the Old Vehicle

Explanation:

Step 1: Consider the relevant transaction from the old vehicle

The Purchase price of the old vehicle is considered a historical cost and in most situations, especially for accounting purposes, this amount has undergone depreciation from the very first year the old vehicle was bought.

Instead of concentrating on the purchase price of the old vehicle, the only transaction from that old vehicle that is worth considering is the Proceeds from its disposal which can serve as part of the payment for the new fire truck to be purchased.

Step 2: Consider the relevant transactions for the new vehicle

One of the very first transactions that are relevant for the new vehicle is the purchase price. A very expensive new fire truck can cancel out the benefits of its acquisition since the main essence of acquisition is to save cost.

Step 3: Consider the Expected Operating Expenses that can be saved by the new truck

This the main reason advanced by the CIty of San Diego to get a new fire truck. Hence, a fire truck that tends to increase maintenance and operating cos will not fit into the decision.

Based on these explanations, therefore, the only transaction that is not relevant to this decision is the purchase price of the old vehicle

Answer:

See below

Explanation:

Given the above, we will use the below to get the factory overhead

Ending finished goods = Opening balance + Direct materials + Direct labor + Factory overhead - Goods finished during the month

Fixing the values, we will have

= $14,600 + $91,700 + $186,600 + Factory overhead -

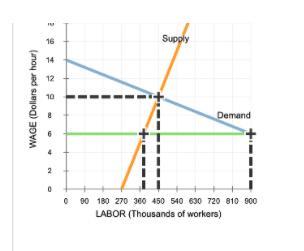

Answer:

The equilibrium hourly wage is the wage where the curve of supply of labor intersects with that of the demand for labor. The same goes for the equilibrium quantity of labor.

The equilibrium hourly wage is <u>$10</u>, and the equilibrium quantity of labor is <u>450 thousand workers</u>.

If a Senator introduces a minimum hourly wage, this is considered a <u>Price Floor. </u>

Price floors are prices that that the government mandates that one cannot charge below for a good or service. If there is a price floor on cake for instance, a person is not allowed to charge less than that price floor for cake. The Senator's bill is therefore saying that people should not be paid less than $6 an hour.

Answer:

he or she can potentially lose 100% of the principal amount due to a stock price decline.

Explanation:

The elderly investor is trying to invest in bluchip stocks that have high returns in order to recoup losses from his previous investment.

Generally the higher the returns on an investment the higher the risk of that investment. Investors are likely to lose their capital in higher yield investments.

A reverse convertible note is a product that is the obligation of the issuing bank and not the corporation. So if price falls below the knock in price, customer will only receive the stock at maturity and not at par. The stocks received could be worthless and investor could loose all his principal.

Answer:

perfect competitor

Explanation:

Given:

Firm's total revenue when 10 units are sold = $100

Firm's total revenue when 11 units are sold = $110

Average Revenue =

or

Average Revenue =  = $10

= $10

and,

the marginal revenue = $110 - $100 = $10

Since,

the average revenue and the marginal revenue for the firm is equal,

therefore, the is a perfect competitor