Answer:

c.a $1,000 bond sold for $1,012.50.

Explanation:

We assume the par value is $1,000 and since the bond is issued at 101.25 that means its selling price is

= $1,000 × 101.25%

= $1,012.50

Since the bond is issued more than the face value that reflects the premium and if the bond is issued less than the face value so it is issued at a discount

So the right option is c.

Answer:

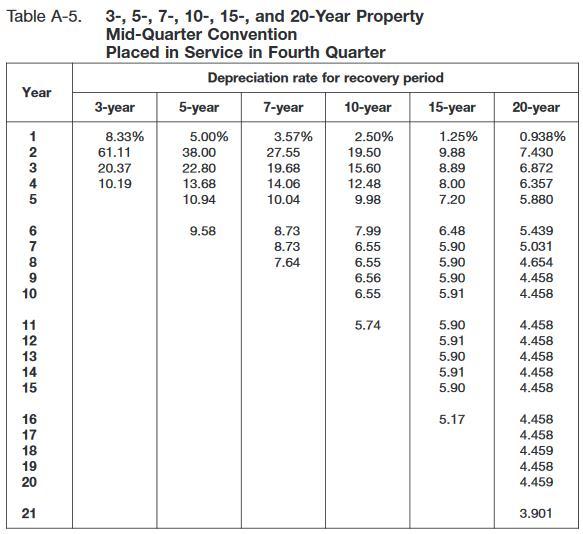

the depreciation expense on the equipment will be 1,785 for tax purpose.

Explanation:

We will look into the MACRS (Modified Accelerated Cost Recovery System)

table for a property of seven years placen into service in the 4th quarter:

Which give us 3.57%

now we multiply the basis by the coefficient and get the value for depreciation

50,000 x 3.57% = 1,785 depreciation expense under MACRS

Answer:

Required return 10.27%

Dividend yield 5.77%

Expected capital gains yield 4.5%

Explanation:

Calculation for required return using this formula

A. R = (D1 / P0) + g

Let plug in the formula

Required return = ($2.30 / $39.85) + .045

Required return = .1027*100

Required return= 10.27%

Therefore Required return is 10.27%

Calculation for dividend yield using this formula

Dividend yield = D1 / P0

Let plug in the formula

Dividend yield = $2.30 / $39.85

Dividend yield = .0577*100

Dividend yield = 5.77%

Therefore Dividend yield is 5.77%

Calculation for the expected capital gains yield

Using this formula

Expected capital gains yield=Required return-Dividend yield

Let plug in the formula

Expected capital gains yield=10.27%-5.77%

Expected capital gains yield=4.5%

Therefore Expected capital gains yield is 4.5%

Answer:

$937,800

Explanation:

The adjusting entry would be

Salaries expense A/c $12,800

To Salaries payable A/c $12,800

(Being salary is adjusted)

The salaries expense is computed below:

= Total five days × number of days ÷ total number of days

= $32,000 × (2 ÷ 5)

= $12,800

Now the ending balance of salaries expense would be

= Unadjusting balance + adjusting balance

= $925,000 + $12,800

= $937,800

Answer:

The yield to call for this bond is 9.30%

Explanation:

Yield to call

The rate of return bondholders receives on a callable bond until the call date is called Yield to call.

Now use the following formula to calculate the Yield to call

Yield to Call = [ C + ( F - P ) / n ] / [ ( F + P ) / 2 ]

Where

F = Face value = $1,000 ( Assumed )

C = Coupon Payment = Face value x Coupon rate = $1,000 x 10.4% = $104

P = Call price of the bond = Face value + Call Premium = $1,000 + $75 = $1,075

n = Numbers of years to call = 10 years

Placing vlaues in the formula

Yield to Call = [ $104 + ( $1,000 - $1,075 ) / 10 years ] / [ ( $1,000 + $1,075 ) / 2 ]

Yield to Call = 0.0930

Yield to Call = 9.30%