It is true that this change would probably be a good move, as it would increase the ROE from 7.5% to 13.5%.

<u>Explanation:</u>

Equity multiplier is calculated by dividing the total assets of a company to shareholder’s equity of an organization. If a company has not raised any debt, then such company would be having equity multiplier equal to 1. t is a leverage ratio.

Return on equity is another financial measure to calculate the return. It is calculated by dividing the net income of a company to the shareholder’s equity. It directly shows the amount that a company is earning on its money invested by the equity shareholders.

Answer: hello your question is poorly structured attached below is the missing graph and missing part of the question

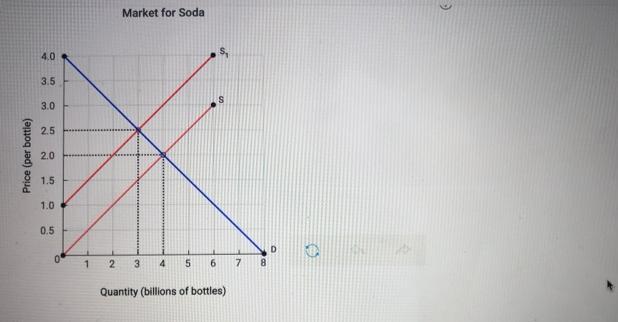

Assume the government imposes a $1.00 excise tax on the sale of every 2 liter bottle of soda. The tax is to be paid by the producers of soda. The figure below shows the annual market for 2 liter bottles of soda before and after the tax is imposed.

answer :

a) $2 , 4 billion

b) $2.5

c) $1.5

d) 3 billion

e) $3 billion

Explanation:

a) equilibrium price = $2 per bottle

equilibrium quantity = 4 billion bottles

<u>b) After imposition of excise tax </u>

consumers will pay = $2.5

<u>c) The amount producers keep after the imposition of taxes </u>

= $2.5 - tax

= 2.5 - 1 = $1.5

<u>d) New equilibrium quantity ( after tax is imposed ) </u>

= 3 billion bottles ( from graph attached ) i.e. intersection of S2 and D

e)<u> Amount of tax revenue collected by the government from the imposition of tax </u>

= quantity of bottles sold * $1

= 3 billion * $1 = $3 billion

Answer:

C. Education and communication.

Explanation:

Since in the question it is mentioned that the resistance to change depend upon the non-sufficient, not correct or the information that misleads so here the managers should use the education & communication for managing the resistance as the given situation represent the education and communication scenario.

Therefore the same is to be considered

hence, the correct option is B.

Mercantilism is the name of the theory

Answer:

He must deposit $10,168.07 per year to reach the future value of $1,000,000.

Explanation:

Giving the following information:

Final value= 1,000,000

n= 25

Interest rate= 10%

We need to calculate the annual deposit necessary to reach the goal of $1,000,000.

To calculate the annual deposit, we need to use the following variation of the future value formula:

FV= {A*[(1+i)^n-1]}/i

A= annual deposit

Isolating A:

A= (FV*i)/{[(1+i)^n]-1}

A= (1,000,000*0.1) / [(1.10^25) - 1]

A= $10,168.07

He must deposit $10,168.07 per year to reach the future value of $1,000,000.