Answer: network structure

Explanation:

Network structure is a form of organizational structure that is considered to be less hierarchical and also more flexible than most other organizational structures. In a network structure, it is the managers who usually both the internal and external relationships.

Barcelona has a core staff of restaurant managers and head chefs and contracts with staffing agencies to fill all other positions, from accountants to dishwashers, then the company has a network structure.

Answer:

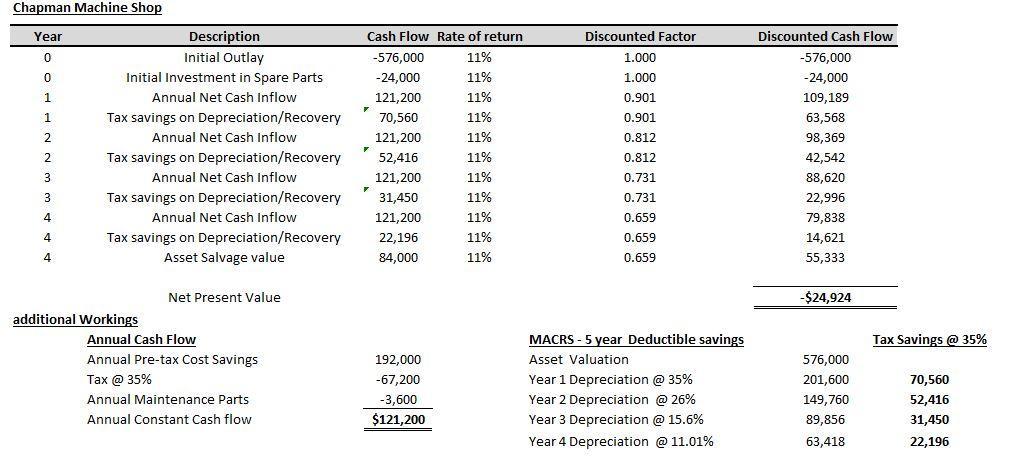

The Firm should not Buy and Install the press as it delivers a negative NPV of -$24,924 at 11% discount rate over its 4 year operations

Explanation:

The General rule is to appraise the investment based on various appraisal techniques.

A technique that should be considered must have special focus on the time value of money, the required rate of returns expected by the firm and other Cashflow considerations.

The Net Present Value (NPV) approach will be the best method to proceed with.

The NPV approach typically falls under the following decision tree:

a. If NPV is negative (Reject the proposal)

b. If NPV is positive (Accept if it's a singular project, Accept the highest positive NPV if it's for mutually exclusive Projects)

c. If Zero (this is the breakeven line at which the Project covers all its cost but does not return a profit.) Also referred to as the IRR

Kindly refer to the attached for detailed workings

When performing data acquisition for an investigation, the component does an engineer acquire first is: "Disk controller cache"

<h3>

What is data acquisition?</h3>

Data Acquisition is synonymous with data collection; it is defined as the process of gathering, filtering, and cleaning data prior to storing it in a data warehouse or other storage solution.

Hence the Disk controller cache will be looked at first because it will contain details and logs of all events that have occurred in that system.

Learn more about data acquisition at;

brainly.com/question/14701948

#SPJ1

Answer:

interest group

Explanation:

Based on the information provided within the question it can be said that this is an example of an interest group. This term refers to group of individuals that share a common interest and because of it work in unison in order to influence the government so that they promote and protect that interest. Which in this scenario the group's main interest is on the food selection in the cafeteria, and are working together to influence the organizational entity to change it.