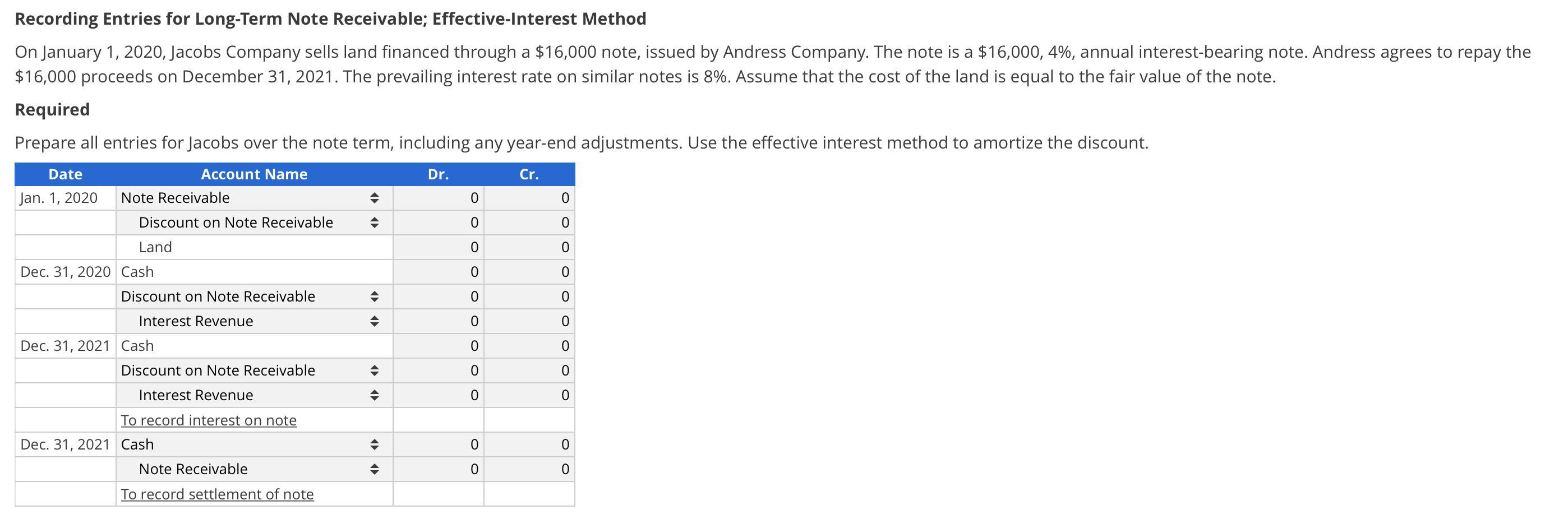

Answer:

Note: <em>See attached picture for journal entry schedule for the question</em>

<em />

Fair Value of Land = -PV(I, N, PMT, FV, Type)

Fair Value of Land = -PV(8%, 2, 16000*4%, 16000, 0)

Fair Value of Land = -PV(8%,2,640,16000,0)

Fair Value of Land = $14,859

Journal Entry

Date Account tile and explanation Debit Credit

Jan. 1 Notes Receivable $16,000

To, Discount on Notes $1,141

To, Land $14,859

Dec. 31 Cash $640

Discount on Notes $549

To, Interest Revenue (14859*8%) $1,189

Dec. 31 Cash $640

Discount on Notes $593

To, Interest Revenue (14859+549)*8% $1,233

Dec. 31 Cash $16,000

To, Notes Receivable $16,000