Answer: See attachment

Explanation:

Note:

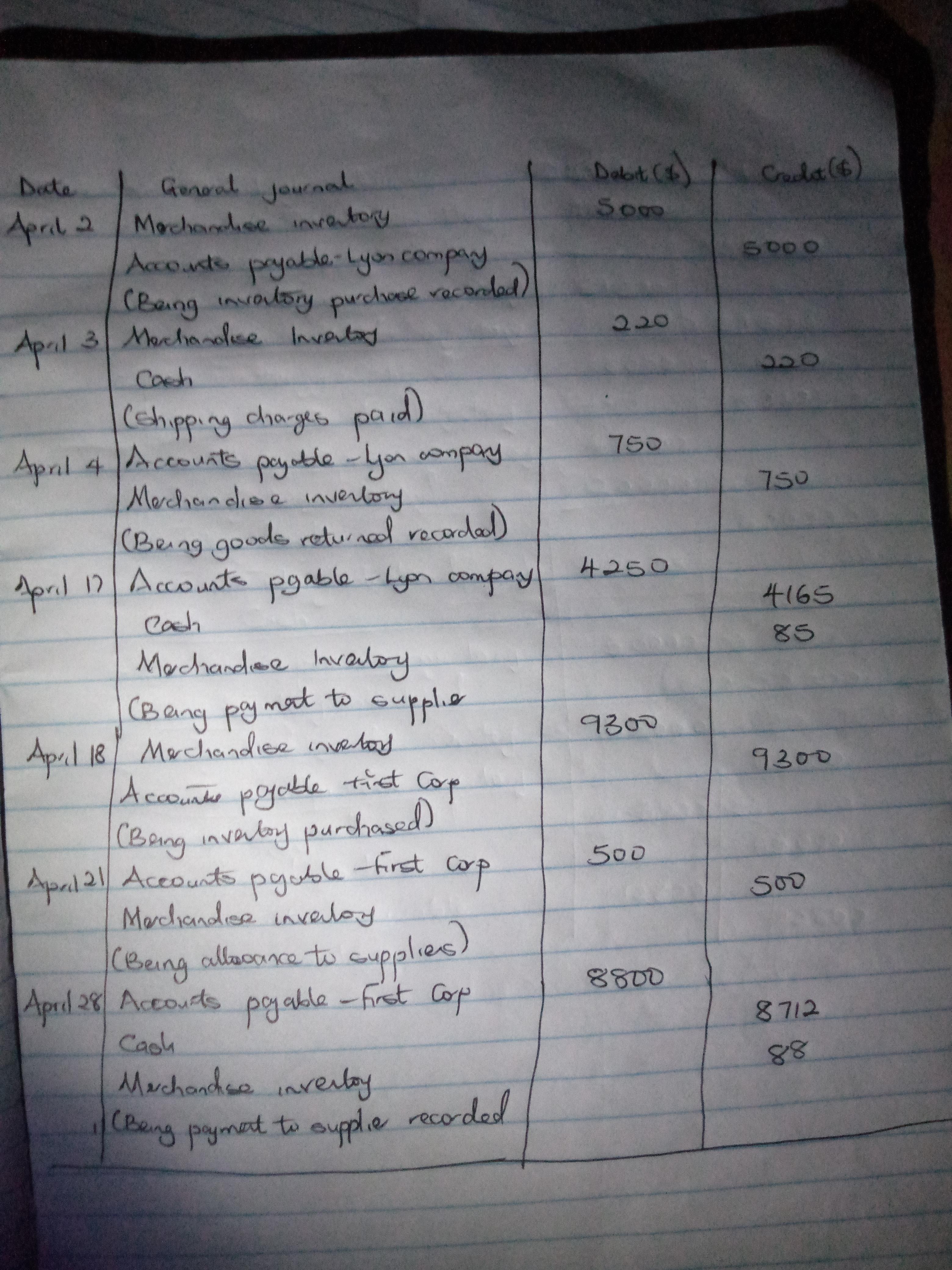

April 17:

Account payable- Lyon Company:

= $5000 - $750

= $4250

Merchandise inventory:

= $4250 × 2%

= $4250 × 0.02

= $85

Cash = $4250 - $85

= $4165

April 28:

Account payable- Frist Corp:

= $9300 - $500

= $8800

Merchandise inventory:

= $8800 × 1%

= $8800 × 0.01

= $88

Cash = $8800 - $88

= $8712

Check the attachment for further information

Answer:

Option A Creating Product Differentiation

Explanation:

The reason is that in the growth stage the company must add further features to the product to increase the product life and also capture the additional market share. This will only be possible if we have product differentiation.

The option D says that using anti-competitive strategy will give advantage to companies but this is not true, the reason is that the entrants enter the market when the product is at mature position (Normally). But this is not true in all situations.

So the best option is A

Answer: See explanation below for answer. The options are:

A. $13,000

B. $ 5,000

C. $18,000

D. $14,000

Explanation:

A taxpayer can deduct the medical expenses that have been paid for a child at the time of adoption if the child should qualify as the dependent of the taxpayer when the medical expenses were paid.

In addition, should a taxpayer pay an adoption agency for the medical expenses that the adoption agency has already paid, then the taxpayer is treated as though he/she has already paid those expenses.

In the scenario given above, Mr. and Mrs. Sloan can deduct the child's medical expenses of $5,000 that they have paid.

But on the other hand, the legal expenses of $9,000 and agency fee of $4,000 that were incurred in during the adoption process will be treated as nondeductible personal expenses.

However, Mr. and Mrs. Sloan will be able to claim a nonrefundable tax credit amounting up to $13,570 for these qualified adoption expenses.