False. Things like volcanoes can cause the greenhouse effect.

If the number is 12,759 and they ask to round to the nearest 10,000 then you look at the thousands place (where the 2 is) and is its less than 5 round down and if its more round up. so the answer would be 10,000

Answer:

are equal to it's domestic production

Explanation:

A country's Gross Domestic Product (GDP) is defined as value of all goods and services produced in a country during a given time. Domestic production refers to those goods and services produced at home for local consumption.

Expenditure refers to the monies expended by all entities namely; household, firms and government on goods and services with a country.

When all the entities involved in generating a country's GDP spend their money towards purchasing goods and services produced in a country, then local producers would have more money to buy materials that will be used for further production. The higher the money spent, the higher the production and vice versa.

The above is a cycle that is repeated each time household, firms and government buys locally produced goods hence expenditure on a nation's domestic production equal to it's domestic production.

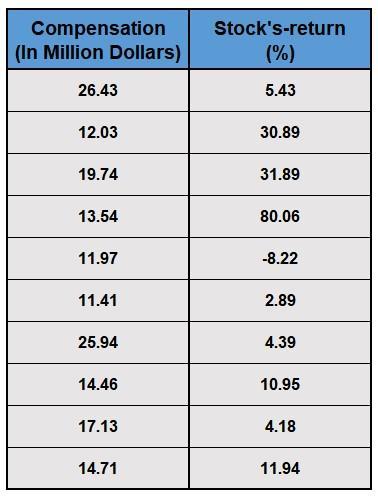

Missing Question Data:

As the Question is missing relevant data, I have searched for it online and found a question similar. The data is attached in a picture file. It might be a little different from your actual question but same approach can be used to solve the question.

Answer with Explanation:

For simplicity, we denote the compensations with variable <em>x </em>and the stock return with variable <em>y.</em> Let us first find the mean and standard deviation for both compensation (x) and return (y).

Mean of Compensation (<em>x) </em> will be,

Mean of Stock Return (y) will be,

Standard Deviation for Compensation (x) is given by,

Standard Deviation for Compensation (x) is given by,

To find the predicted stock return, we have to use the equation for of line of regression,

where,

Equation (1) will become,

.

.