Answer:

a. marginal revenue in the peak period is greater than in the off-peak period.

Explanation:

<u>peak-load pricing:</u> The price increase when the demand of the good is at peak, so at higher demand the price is higher. Later when the good demand decrease, the price will decrease.

The consumer who purchases at peak pays more compared to another who acquire the good during off-peak periods.

<u>marginal revenue: </u>revenue generated for the sale of another unit

The company will set the marginal revenue equal to marginal cost.

On peak the demand increase along with the marginal cost.

So if marginal revenue = marginal cost

and marginal cost peak > marginal cost off-peak

we can declare:

marginal revenue peak > marginal revenue off-peak

Answer:

1. 2,584

Explanation:

future payments: $1,000 in 1 year and $2,000 in 3 years

the present value of alternative I (one year bond):

$1,000 / 1.06 = $943.40

the present value of alternative II (first 2 years and then 1 year):

$2,000 / 1.065 = $1,877.93 ⇒ PV at year 2

PV at year 0 = $1,877.93 / 1.07² = $1,640.26

the total present value of both options = $943.40 + $1,640.26 = $2,583.66 ≈ $2,584

Correct/Complete Question:

Broker Needa leaves for vacation. In his absence, associate Wanna will be handling the escrow accounts. If Wanna errors with the accounting procedures:

A. Broker Needa's license will be revoked

B. Broker Needa's vacation may be permanent as he is ultimately responsible

C. The Commission will excuse Needa and Wanna; everyone needs a vacation

D. Broker Wanna's solely responsible for her actions

Answer:

B. Broker Needa's vacation may be permanent as he is ultimately responsible

Explanation:

Since Broker Needa is the employer of Wanna, he is ultimately responsible for the errors as the assistant works under his license. Brokers are always responsible for agents under their license.

I hope this helps.

In every business they try to spark peoples eyes they wanna get consumers attention so they add Dasani drops and Dasani sparkling to get there attention so that people will invest into there product

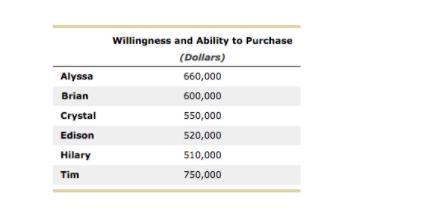

Answer:

a) will

d) crystal

Explanation:

Please find the information needed to answer this question in the attached image

Willingness to pay is the highest amount a consumer would be willing to buy a product. If the price of the good is below the willingness to pay, the consumer would purchase the good.

The three beachfronts were sold to Alyssa, Tim and Brian.

The new sale of the beachfront at $535,000 would be sold to crystal because her willingness to pay ($550,000) is higher than the price of the beachfront.

the consumer surplus from the purchase would be $550,000 - $535,000 = $15,000