Answer:

Medicare

Explanation:

I think b because we can only get it free on very poor and undeveloped are but it cost high in developer area

Answer:

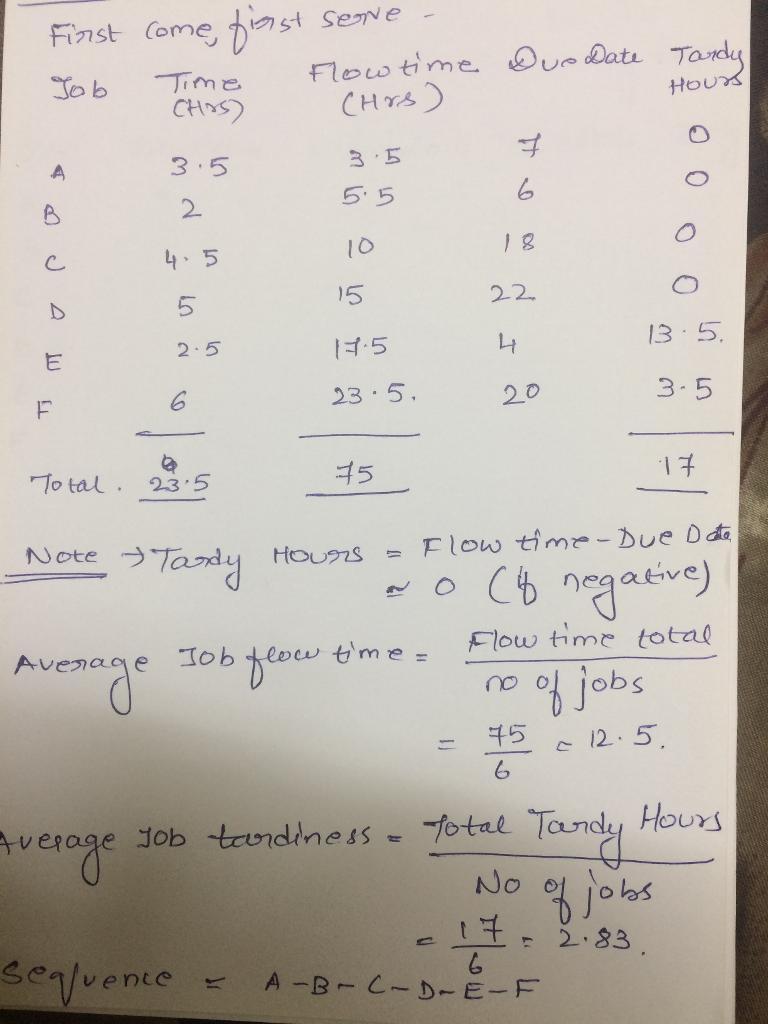

Job sequence

First come first serve = a - b-c-d-e-f

Shortest processing time = b-e-a-c-d-f

Earliest due date = e-b-a-c-f-d

Critical ratio = e-a-b-f-c-d

First come first serve Shortest processing time Earliest due date Critical ratio

Average flow time 12.5 11.33 11.58 12.08

Avg Job tardiness 2.83 0.83 0.42 0.67

Find attachments for complete answer

Answer:

True

Explanation:

A more precise way to describe the situation is that Joe's pizza parlor is a monopolistic competition. But that definition considers that all 'food' items have some degree of close substitute relation.

But yes, if you consider this two conditions:

- a broad definition of monopoly

- other restaurants are not considered close substitutes for the food sold at the pizza parlor

Then yes, Joe has monopoly

Answer:

<u>Scholarship Amount would be $45.68</u>

Explanation:

Deposits into an endowment account that pays 12% per year

Year 0 Deposit $100

Year 1 Deposit $90

Year 2 Deposit $80

Year 3 Deposit $70

Year 4 Deposit $60

Year 5 Deposit $50

Year 6 Deposit $40

First find the present worth of the gradient deposits.

P = 100 + 90(P/A, 12%, 6) - 10(P/G, 12%, 6) = $380.69

A = 380.69 (0.12)

A= $45.68

Privileged-level access is granted to authorized personnels that could affect the important files, data, network communications, etc. In the provisions of the Information Security and Policy, privileged access may be given to authorized management accounts. However, they still have to follow the guidelines and procedures of the organization.

The answer is letter D.