Answer:

202%

Explanation:

Calculation to determine what the company's overhead application rate is

First step is to calculate the Total manufacturing overhead using this formula

Total manufacturing overhead = Overhead rate - Direct material cost - Direct labor cost

Let plug in the formula

Total manufacturing overhead =5220 - 2,200 - 1000

Total manufacturing overhead =2020

Now let determine the overhead application rate using this formula

Overhead application rate=Total manufacturing overhead/Direct labor cost

Let plug in the formula

Overhead application rate=2020/1000*100

Overhead application rate=202%

Therefore, the company's overhead application rate is:202%

Answer:

12 months

Explanation:

The fiscal or financial period of a business lasts for 12 months or one year. It means that at the end of that 12 months, the business prepares its financial statement to determine its profitability. The business assesses its growth, success, and failure for the period.

After evaluating performance, planning for the next period of 12 months begins. The entrepreneur prepares a budget for the year, including their compensation. Compensation for the entrepreneur should be budgeted and reviewed every year together with the other budget items.

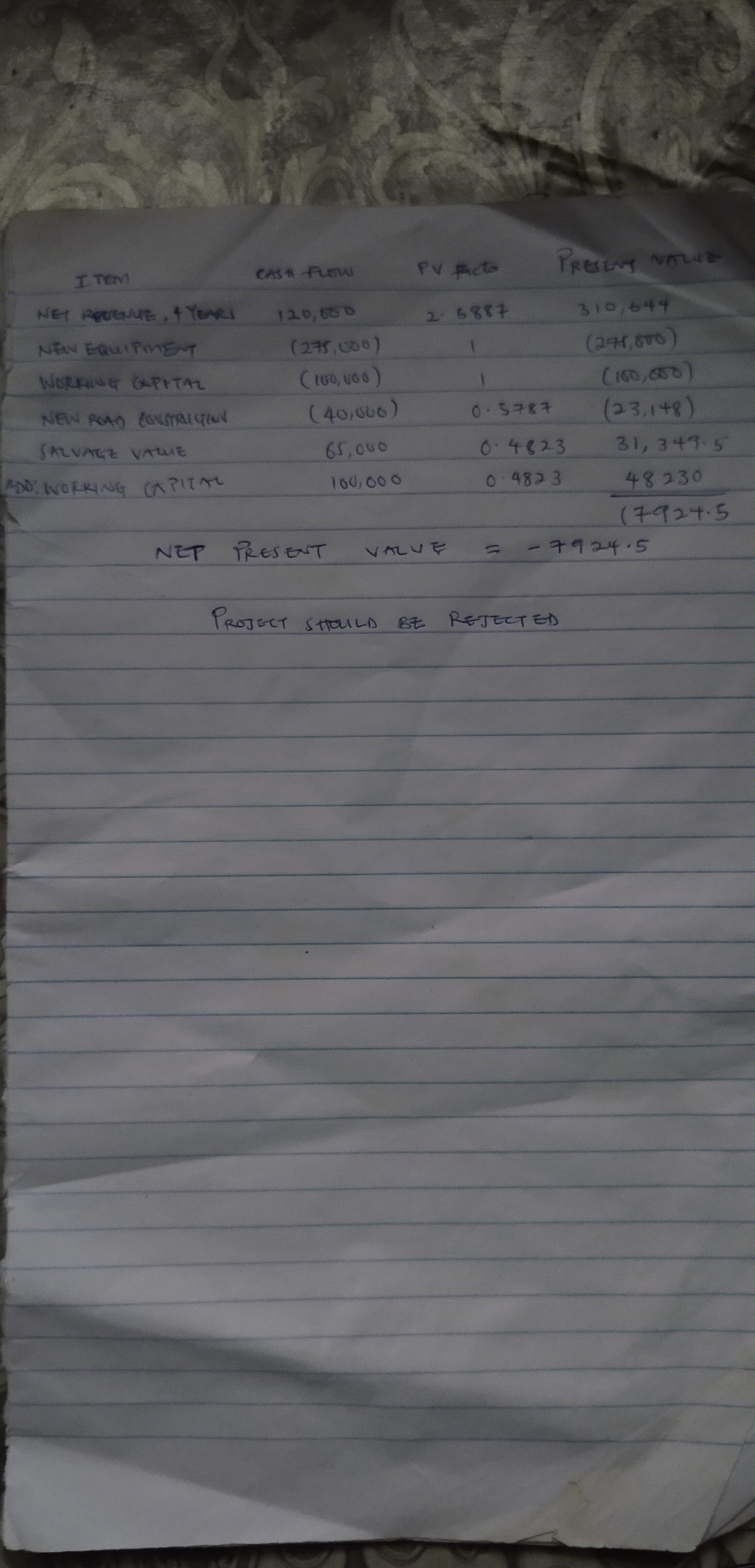

Answer: $7924. 5

Explanation:

Given the following :

Cost of new equipment and timbers - $275,000

Working capital required - $100,000

Annual net cash receipts - $120,000

Cost to construct new roads in year three - $40,000

Salvage value of equipment in four years - $65,000

Kindly check attached picture for Explanation

Commission means that an employee is paid a given amount regardless of the number of hours worked or quality of the work.

Answer: interest tax shield

Explanation: A tax shield is a reduction in taxable income for an individual or corporation achieved through claiming allowable deductions such as mortgage interest, medical expenses, charitable donations, amortization, and depreciation .

The term “interest tax shield” refers to the reduced income taxes brought about by deductions to taxable income from a company’s interest expense. For instance, there are cases where mortgages may have an interest tax shield for buyers since the mortgage interest is deductible against income. One of the main objectives of companies is to reduce their tax liability as much as possible. Interest tax shields encourage firms to finance projects with debt, since the dividends paid to equity investors are not deductible.