Answer:

When Manufacturing of a Product involves several processes.

Explanation:

When several processes are involved in manufacturing a product, costs need to be accumulated in these processing departments. Thus, A process cost accounting system is most appropriate

<span>Food service operators must pay attention to detail and watch their finances in order to maximize the profit they can generate through the operation of their business. There are many aspects of a food service business that have potential to be a loss, so operators must be aware of these aspects - such as loss from ordering too much food or ingredients, employee theft, and so on.</span>

The interest expense for the year ended December 31, 2021, for Blanchard Corporation is b) $9,000.

<h3>How is interest expense computed?</h3>

Interest expense is prorated. Since Blanchard Corporation issued the notes on April 30, the interest expense for the year will not be for 12 months but only 8 months (May to December).

<h3>Data and Calculations:</h3>

Note payable = $150,000

Interest rate = 9%

Period of note = 1 year

Date of issuance = April 30, 2020

Interest expense at December 31, 2021 = $9,000 ($150,000 x 9% x 8/12)

Thus, the interest expense for the year ended December 31, 2021 is b) $9,000.

Learn more about interest expense at brainly.com/question/16134508

Answer:

(D) - It engages in Foreign Direct Investment, which by itself raises US net capital outflow

Explanation:

Foreign Direct Investments (FDIs) are investments in physical assets, infrastructures, etc and other long-term assets made in a foreign country. They differ from Foreign Portfolio Investments (FPIs) which are investments in stocks, bonds, treasury securities and other listed securities which can be sold easily in financial markets. For instance, when a US-based corporation invests in the stocks or bonds of a French company, this is FPI. Whereas, when the US-based corporation establishes a company in France by investing as plants and machinery, this is FDI.

FDIs requires cash commitment for investing in the foreign nation. However, because the assets created as a result of these investments are owned by the originating country, it increases the volume of assets the country has abroad leading to an increase in net capital outflow. Net Capital Outflow is the volume of capital investment made by a nation in other countries, less the capital investment made by other countries into the nation.

Therefore, when Stryker builds and operate a new factory in France, it engages in Foreign Direct Investment. By itself this action raises US net capital outflow.

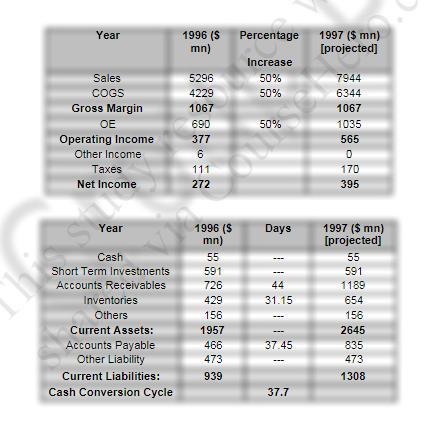

Dell can fund this growth internally by:

- The $469 million increase in current liabilities serves as a source of funds.

- The estimated increase in net profits to $395 million is approximately $123 million.

- The short-term investment is assumed to be the same as in 1996, namely $591 million.

<h3>

What is funding?</h3>

- Business financing is a funding option that allows business owners to obtain business loans to cover expenses such as temporary cash flow interruptions, expansion projects, stock and equipment, and seasonal spikes in activity.

- Retained earnings, debt capital, and equity funding are the three major sources of corporate financing.

So, according to the given chart:

- As a result, an additional operating asset of $794 million is required to sustain growth.

- The $469 million increase in current liabilities serves as a source of funds.

- The estimated increase in net profits to $395 million is approximately $123 million.

- The short-term investment is assumed to be the same as in 1996, namely $591 million.

- As a result, we can confidently predict that growth will be funded internally.

Therefore, Dell can fund this growth internally by:

- The $469 million increase in current liabilities serves as a source of funds.

- The estimated increase in net profits to $395 million is approximately $123 million.

- The short-term investment is assumed to be the same as in 1996, namely $591 million.

Know more about funding here:

brainly.com/question/25887038

#SPJ4