For the answer to the question above,

It is multiple choice letter a. Face Value

In layman's term face value is the nominal value of a security of the issuer or stocks, it is the original cost of the stock shown on the certificate. For bond i<span>t is the </span>amount<span> paid to the holder at maturity.

</span>

Answer:

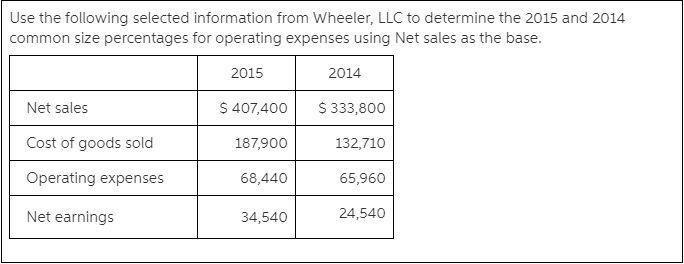

19.8%; 16.8%

Explanation:

In 2016:

Common size percentages for operating expenses:

= (Operating expenses ÷ Net sales) × 100

= (65,960 ÷ $333,800) × 100

= 0.198 × 100

= 19.8%

In 2017:

Common size percentages for operating expenses:

= (Operating expenses ÷ Net sales) × 100

= ($68,440 ÷ $407,400) × 100

= 0.1680 × 100

= 16.8%

Note:

Table is missing in this question, so i have attached the missing table.

Answer:

The answer is A. A Self employed person

Explanation:

An entrepreneur is a creative and innovative individual that generates idea and new invention and takes risk relating to a business entity with the hope that it will yield profit.

An entrepreneur manages a business enterprise with usually considerable initiative or risk. Entrepreneurs are self employed and own their business enterprise and bring new products and services to the market by seizing opportunities.

From the explanation of who an entrepreneur is the best possible option is A. A Self employed person

Answer:

Season:

Fall 262 units

Winter 391 units

Spring 178 units

Summer 569 units

Explanation:

First, we calculate the average for each season.

Then, we cross multiply for 1,400 radials to get the values:

![\left[\begin{array}{cccc}Season&Y_1&Y_2&Average\\$fall&250&200&225\\$winter&320&350&335\\$spring&160&145&152.5\\$summer&635&340&487.5\\\\$total&1035&1365&1200\end{array}\right]](https://tex.z-dn.net/?f=%5Cleft%5B%5Cbegin%7Barray%7D%7Bcccc%7DSeason%26Y_1%26Y_2%26Average%5C%5C%24fall%26250%26200%26225%5C%5C%24winter%26320%26350%26335%5C%5C%24spring%26160%26145%26152.5%5C%5C%24summer%26635%26340%26487.5%5C%5C%5C%5C%24total%261035%261365%261200%5Cend%7Barray%7D%5Cright%5D)

Now we cross multiply to get the expected sales for Year 3:

225 / 1200 * 1400 = 262

335/ 1200 * 1400 = 391

152.5/ 1200 * 1400 = 178

487.5/ 1200 * 1400 = 569