Answer: The correct answer is choice A - a huge increase in the monetary base.

Explanation: From before the financial crisis began in September of 2007 to when the crisis was over at the end of 2008, the amount of Federal Reserve assets rose, leading to a huge increase in the monetary base.

Answer:

Explanation:

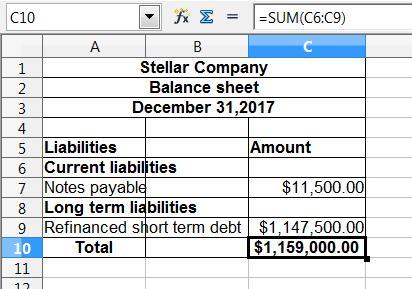

Before showing how short term debt should be presented before doing this we have to classify the items in each head

Like - In current liabilities, notes payable is recorded at $11,500

And, in the long term liabilities, the proceed after brokerage fees for $1,147,500 should be recorded.

The total amount would remain the same i.e $1,159,000

Kindly find the attachment below:

Answer:

The standard deduction is a specific dollar amount that reduces your taxable income. For the 2021 tax year, the standard deduction is $12,550 for single filers and married filing separately, $25,100 for joint filers and $18,800 for head of household.

Explanation:

Answer:

Macau

Explanation:

First, we need to understand that all countries are impacted financially due to the corona virus. It's predicted that Corona Virus will cause a loss of around $2.7 trillion in Global Economy.

That being said, some countries are impacted more than the others.

Especially those who rely on tourism and hospitality as their main economy. Macau is probably the one that got the hardest hit. Not only this country is located near China (where the virus originally came from) , tourism and hospitality accounted for around 43% of Macau's economy. Basically half of its economic activity shut down due to the virus.