Break-even analysis for a service company involves unit of analysis.

What is Break-even analysis?

Break-even analysis calculates a company's margin of safety and compares it to the revenue the company generates and its associated costs. In other words, the analysis shows the turnover required to cover operating costs. Break-even analysis determines the level of revenue required to cover the company's total fixed costs by analyzing different price levels in relation to different levels of demand. A seller's selling power is revealed to a large extent by demand-side research.

To learn more about Break-even Analysis

brainly.com/question/9212451

#SPJ4

Answer:

Explanation:

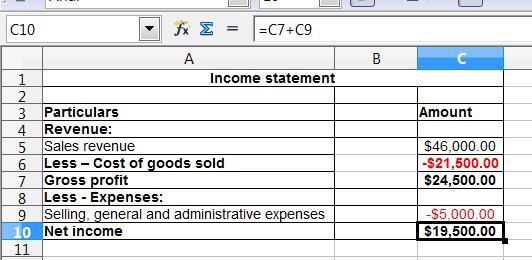

(a) The computation of the cost of goods sold is shown below:

= Beginning inventory + Purchase of new merchandise - ending inventory

= $4,000 + $22,000 - $4,500

= $21,500

(b) In the income statement, the total revenues and the total expenses are recorded.

If the total revenues are more than the total expenditure then the company earns net income

And, If the total revenues are less than the total expenditure then the company have a net loss

This net income or net loss would reflect in the statement of the retained earning account.

The preparation of the income statement is presented in the spreadsheet. Kindly find the attachment below:

Answer:

true

Explanation:

if the job gets to you and you mad then when a person needs help me may loose your temp

Answer:

C) reduced standardization of components

Explanation:

Manufacturability and value engineering refers to any improvements made on a product's design and production process, maintainability and proper use.

These improvements focus on reducing environmental impact (more recycled materials, less hazardous components), enhanced job safety and a simpler way of using the product.

Answer:

C. $737,500

Explanation:

The formula to compute the ending balance of retained earning is shown below:

The ending balance of retained earning = Beginning balance of retained earnings + net income - dividend paid

= $659,000 + $220,000 - $141,500

= $737,500

The net income is calculated below:

= Sales revenues - expenses

$600,000 - $380,000

= $220,000