Complete Question:

PB10-2 Recording and Reporting Current Liabilities with Evaluation of Effects on the Debt-to-Assets Ratio [LO 10-2, LO 10-5]

Tiger Company completed the following transactions. The annual accounting period ends December 31.

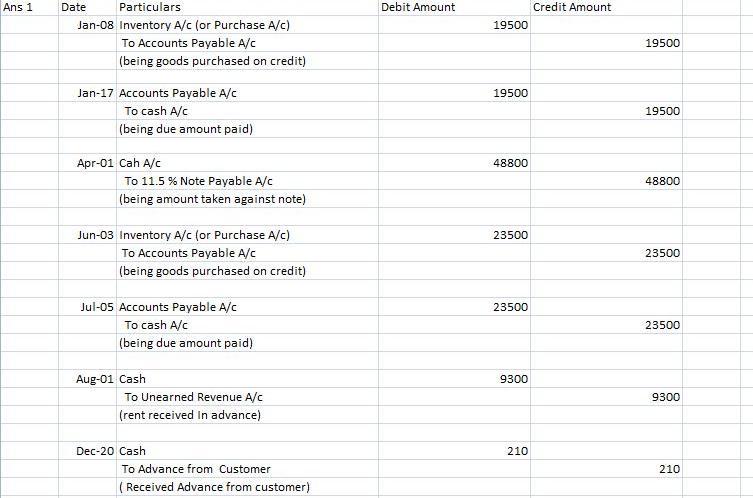

Jan. 3 Purchased merchandise on account at a cost of $24,000. (Assume a perpetual inventory system.) Jan.

27 Paid for the January 3 purchase.

Apr. 1 Received $80,000 from Atlantic Bank after signing a 12-month, 5 percent promissory note.

June 13 Purchased merchandise on account at a cost of $8,000.

July 25 Paid for the June 13 purchase.

July 31 Rented out a small office in a building owned by Tiger Company and collected eight months’ rent in advance amounting to $8,000.

Dec. 31 Determined wages of $12,000 were earned but not yet paid on December 31 (Ignore payroll taxes).

Dec. 31 Adjusted the accounts at year-end, relating to interest.

Dec. 31 Adjusted the accounts at year-end, relating to rent.

Required:

1. & 2. Prepare journal entries for each of the transactions through August 1 and any adjusting entries required on December 31.

3. Show how all of the liabilities arising from these items are reported on the balance sheet at December 31.

Answer:

Prepared journal Entries for Questions 1, 2 and 3 are attached as images in this order

1 Journal Entry Worksheet 1 (image 1)

2 Journal Entry Worksheet 1 (image 2)

3 Journal Entry Balance sheet 1 (image 3)