Answer:

a. Fiscal Policy involves changing <u>government purchases and tax</u>. In the United States, Fiscal Policy is implemented by the <u>federal government</u>.

b. <u>An expansionary fiscal policy </u>can be used to address a Recessionary Gap by<u> </u><u>reducing</u><u> </u>taxes and <u>increasing</u><u> </u>government purchases.

Explanation:

Fiscal policy can be described as the employment of the government purchase and taxation level by the federal goveernment with the aim of influencing the aggregate demand and economic activity level.

Expansionary fiscal policy occurs when the government increases its purchases and reduces taxes in order to close Recessionary Gap, while contractionary fiscal policy is when the government reduces it purchases and increases taxes.

Based on this explanation, we have:

a. Fiscal Policy involves changing <u>government purchases and tax</u>. In the United States, Fiscal Policy is implemented by the <u>federal government</u>.

b. <u>An expansionary fiscal policy </u>can be used to address a Recessionary Gap by<u> </u><u>reducing</u><u> </u>taxes and <u>increasing</u><u> </u>government purchases.

Answer:

B. Surplus and the price level will fall

Explanation:

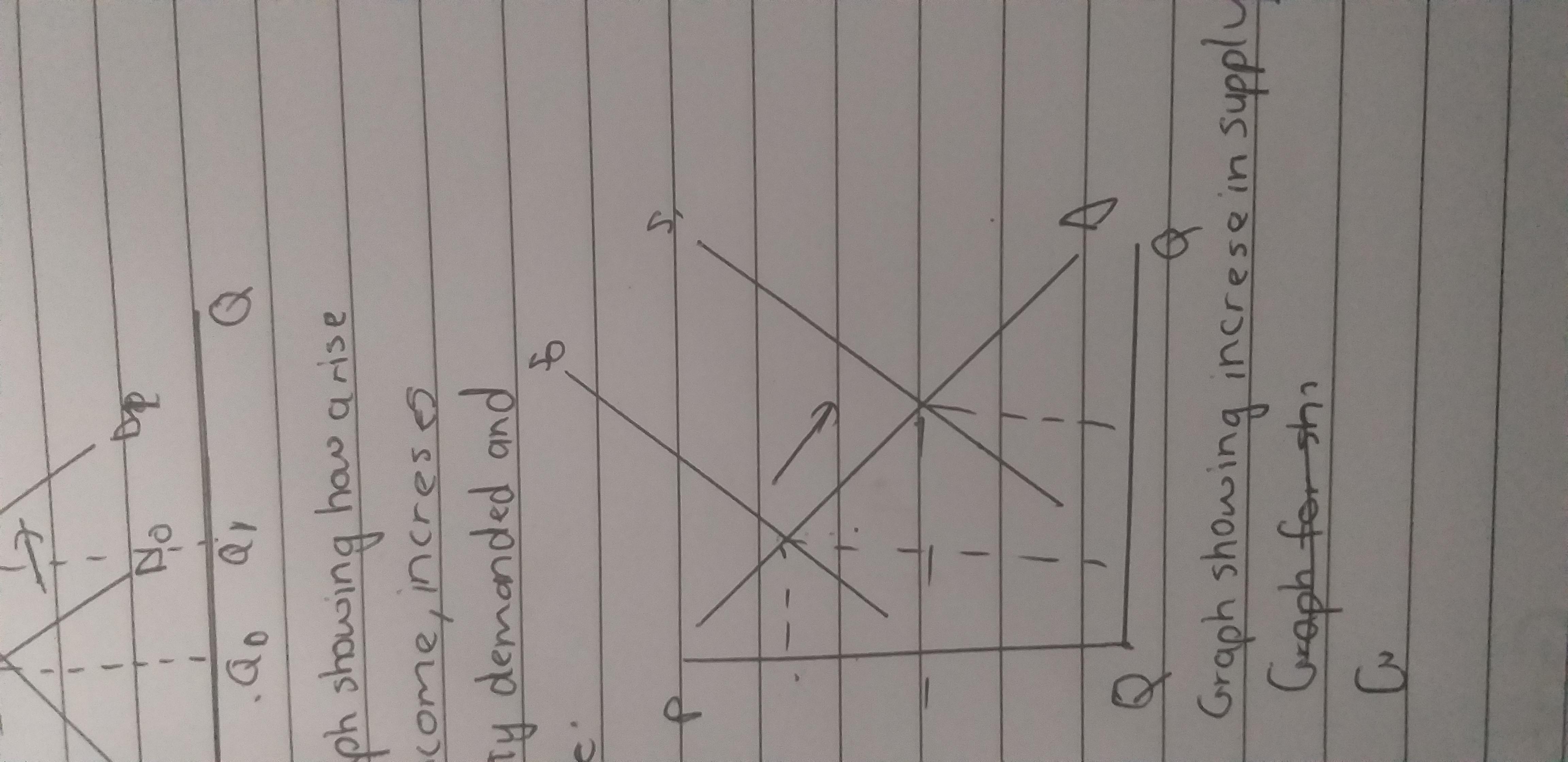

If at a particular price level the real domestic output from producers is greater than real domestic output desired by purchasers it means that supply has outstripped demand and price has not changed.

If supply is greater than demand, there would be a surplus and prices would fall.

An increase in supply is shown by a rightward shift of the supply curve.

The correct answer is A.

Google’s relaxed and non-traditional culture is one aspect of their business model.

Answer:

Superintendent, Principal, teacher, student

Explanation:

Answer: C. $150,000 credit

Explanation:

In the financial statements for year 2, it should be noted that the year 1 retained earnings balance, should be adjusted by $150,000 credit.

The corrections of errors should be treated as the period adjustments before. In this case, the $150,000 overstatement for the cost of goods that was sold in the previous year, will then be credited to the beginning balance of the retained earnings.

Therefore, the correct option is C.