Answer:

the cash that should be freed up is $267

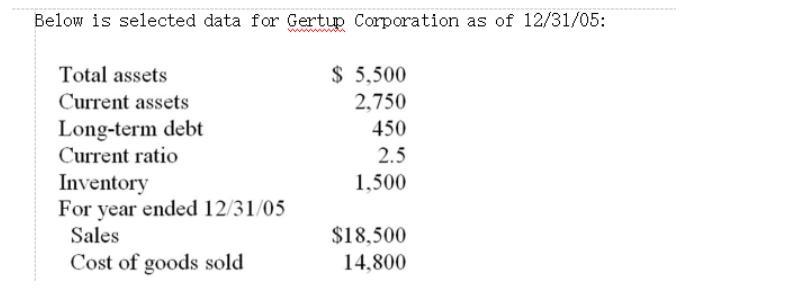

Explanation:

The computation of the cash that would be freed up is shown below:

As we know that

The inventory turnover is

= Cost of goods sold ÷ average inventory

12 = $14,800 ÷ average inventory

So, the average inventory is 1,233

Now the cash that should be freed up is

= 1,500 - 1,233

= $267

hence, the cash that should be freed up is $267

<u>Answer:</u>Option<u> </u>$29,400

<u>Explanation:</u>

The credit items that will be shown on the trial balance are as follows

Accounts payable 2800

Notes Payable 4200

Denton Capital 1400

Revenues 21000

Total Credits in 29400

trial balance

In a trial balance the total debit and credit items should balance. Trial balance has all the items that are posted in the general ledger account. It is a book keeping work sheet that contains the balance of all ledgers. At end of reporting time trial balance is prepared by the company.

Answer and Explanation:

Debit bad debt expense for $40,000 and credit allowance for uncollectible accounts for $40,000

A company's triple bottom line measures environmental, financial, and social. aspects of its performance.

Environmental means relating to or caused by the environment in which a person lives or in which something exists. Protects against environmental influences such as wind and sun. The form that the human family takes is a response to environmental stress.

Financial usually refers to financial matters or transactions of some magnitude or importance. In other words, a financial assistant. Fiscal is used specifically in connection with government or institutional funds. It's the end of the fiscal year. Currency refers specifically to money itself. i.e. currency system or standard.

Relating to interaction with other people especially for pleasure a busy social life.

learn more about the Environmental here. brainly.com/question/1888324

#SPJ4