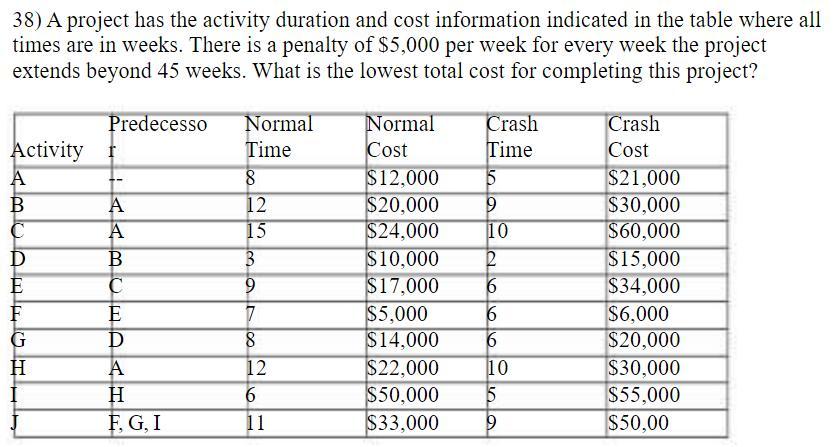

Finishing this job could cost as low as $222,000 in total. If the project is finished in 45 weeks, the final cost will be $400,000. If the project is completed in 46 weeks, the overall cost will be $405,000. The project is finished in 45 weeks, which has the lowest overall cost.

This project can be finished for as little as $222,000 overall. This is so that there is no penalty if the project is finished in 45 weeks. A $5,000 fine is imposed if the project is finished in less than 46 weeks. Thus, completing the project in 45 weeks results in the lowest overall cost. Examining the costs associated with each action is one method to approach this. The first activity will cost $40,000 to complete. The second activity will cost $60,000 to complete. The third activity will set you back $80,000. The fourth action will set you back $100,000. The sixth activity will set you back $120,000. The project will cost $400,000 in total. The overall cost, if the project takes 45 weeks to complete, is $400,000. The whole expense is $405,000 if the project is finished in 46 weeks. Thus, completing the project in 45 weeks results in the lowest overall cost.

To know more about Cost, refer to this link:

brainly.com/question/20534030

#SPJ4

Answer:

The answer is $99700

Explanation:

Net cash from operating activity= Net income + Depreciation - increase in net working capital.

Net cash from operating activity= $96,200 + $6,300 - $2,800= $99700

Answer:

C) for assault and battery, because there was both a threat and a harmful action.

Explanation:

Both assault and battery are crimes but can also result be considered torts and result in civil lawsuits:

- Assault refers to a threat of bodily harm.

- Battery refers to actually harming the other person.

Since both took place in this case, Jill can be charged of both crimes and Jack can also sue her for both torts.

Answer: The strength of a tendency to act in a certain way depends on the strength of our expectation of a given outcome and its attractiveness

Explanation:

The Expectancy Theory defines the efforts of individuals at work. It suggests that people only work as hard as they think is needed for them to get a certain reward or benefit. This is why when there is just a basic salary, employees are not very hard-working but if a car is thrown in as a bonus for the employee of the year, they really put in work.

It therefore shows that the strength to act in a certain way is based on how an individual believes they will be compensated and if that compensation is worth it.

Answer: c. May cause the company's overall weighted average cost of capital to either increase or decrease over time.

Explanation:

Weighted Average Cost of Capital (WACC) as the term implies, is a weighted average of the various rates that the company uses to source capital. If therefore, the company assigns different discount rates based on risk level, WACC will either increase or decrease overtime.

With better discount rates, the WACC will decrease to reflect the lower risk and with worse rates, WACC will increase to reflect the higher risk associated with the company. .