A antonym for delicate could be firm

Complete Question:

Land and other real estate held as investments by endowments in a government’s permanent fund should be reported at

Group of answer choices

A. Historical cost.

B. Fair value less costs of disposal.

C. Fair value.

D. The lower of cost and net realizable value.

Answer:

C. Fair value.

Explanation:

Land and other real estate held as investments by endowments in a government's permanent fund should be reported at fair value of the reporting date except for the exception of life insurance contract, external investment pool, money market investment etc.

The fair value can be defined as the actual or real value of an asset, security, product or item in financial accounting.

Answer:

The correct answer is C. Common fixed costs.

Explanation:

A fixed cost is an expense that the company must incur, even if the company operates at medium speed, or does not, which is why they are so important in the financial structure of any company.

This is the case, for example, of payments such as leasing, since this, if nothing is sold, must be paid. It also happens with almost all labor payments, public services, insurance, etc.

Perhaps the main component of fixed costs is labor, therefore, it is not surprising that companies struggle every day for greater labor flexibility that allows them to convert those fixed costs into variables.

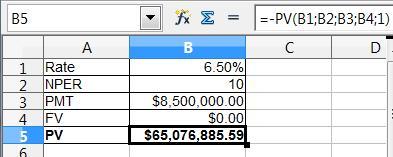

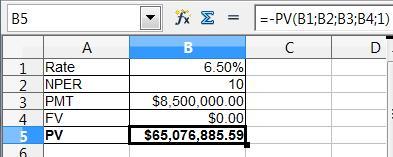

Answer:

A. It will stay the same.

Explanation:

The formula to compute the dividend yield is shown below:

= (Annual dividend ÷ market price) × 100

Since in the question, it is given that the expected dividend is growing at the constant growth rate i.e 6.50%, so the expected dividend yield will remain the same in the future.

As it shows a direct relationship between the growth rate and the dividend yield plus the market price is growing at a steady rate