Answer:

a) The probability that a randomly selected LU graduate will have a starting salary of at least $30,400 = P(x ≥ 30400) = 0.0968

b) The probability that a randomly selected LU graduate will have a salary of exactly $30,400 = 0.000021421

c) Percentage of students that will receive a tax break = 29.12%

d) Total Number of graduates this year = 3,000

Explanation:

This is a normal distribution problem with

Mean = μ = $20,000

Standard deviation = σ = $8,000

a) The probability that a randomly selected LU graduate will have a starting salary of at least $30,400 = P(x ≥ 30400)

We first normalize or standardize $30,400

The standardized score for any value is the value minus the mean then divided by the standard deviation.

z = (x - μ)/σ = (30400 - 20000)/8000 = 1.30

The required probability

P(x ≥ 30400) = P(z ≥ 1.30)

We'll use data from the normal probability table for these probabilities

P(x ≥ 30400) = P(z ≥ 1.30) = 1 - P(z < 1.30)

= 1 - 0.90320

= 0.0968

b) The probability that a randomly selected LU graduate will have a salary of exactly $30,400

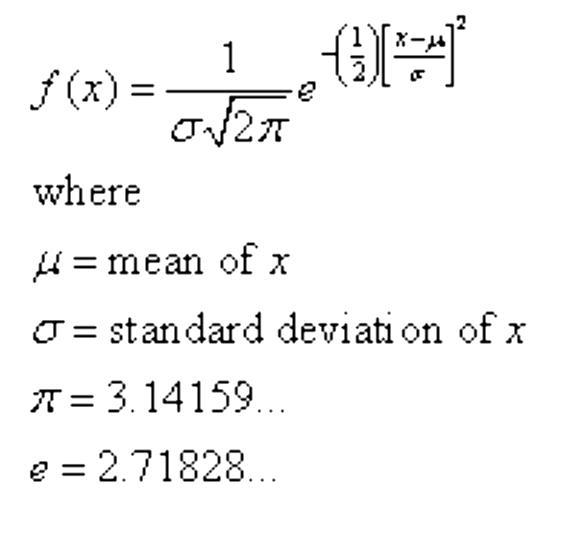

Here, we will use the normal distribution formula. The normal distribution formula is presented in the attached image

P(X = x) = f(x) = [1 ÷ σ√(2π)] × e^(-0.5z²)

x = $30,400

σ = $8,000

z = 1.30

P(X = 30400) = f(30400) = 0.000021421

c) Individuals with starting salaries of less than $15600 receive a low income tax break.

What percentage of the graduates will receive the tax break?

Required probability = P(x < 15600)

We first normalize or standardize $15,600

z = (x - μ)/σ = (15600 - 20000)/8000 = -0.55

The required probability

P(x < 15600) = P(z < -0.55)

We'll use data from the normal probability table for these probabilities

P(x < 15600) = P(z < -0.55)

= 0.29116 = 29.116% = 29.12%

d) If 189 of the recent graduates have salaries of at least $32240, how many students

graduated this year from this university?

We first find the percentage of LU graduates with salaries more than $32240

Required probability = P(x ≥ 32240)

We first normalize or standardize $32,240

z = (x - μ)/σ = (32240 - 20000)/8000 = 1.53

The required probability

P(x ≥ 32240) = P(z ≥ 1.53)

We'll use data from the normal probability table for these probabilities

P(x ≥ 32240) = P(z ≥ 1.53) = 1 - P(z < 1.53)

= 1 - 0.93699

= 0.06301 = 6.301%

So, 6.301% of the graduates this year = 189

Total Number of graduates this year = (189/0.06301) = 2999.5 = 3000 graduates this year.

Hope this Helps!!!