The capital projects fund account for the 10 percent retainage as (B) II only.

<h3>

What is retainage?</h3>

- Retainage is a percentage of the agreed-upon contract price withheld until the work is substantially completed to ensure that the contractor or subcontractor will fulfill its responsibilities and complete a construction project.

- Retention is money kept back by one party in a contract as security for unfinished or defective work.

- Assume the contract is worth $20,000 and you're submitting a paid app after finishing 25% of the work.

- So you earned $5,000 during the pay period, but retainage is 5%. The current progress payment has been reduced by $250.

- As a result, the "Amount Due for this Request" will be $4,750.

So, in the given situation the capital projects fund account for the 10 percent retainage as (II) the credit for $400,000 to Contracts Payable-Retained Percentage, that is (B) II only.

Therefore, the capital projects fund account for the 10 percent retainage as (B) II only.

Know more about retainage here:

brainly.com/question/24101126

#SPJ4

The correct question is given below:

The capital projects fund of Hood River completed the construction of an addition to its city hall at a cost of $4,000,000. The city council approved payment of the amount due to the general contractor, less a 10 percent retainage. How should the capital projects fund account for the 10 percent retainage?

I. As a credit of $400,000 to Deferred Revenue-Retained Percentage

II. As the credit for $400,000 to Contracts Payable-Retained Percentage.

A. I only

B. II only

C. Either I or II

D. Neither I nor II

The formula of the future value of an annuity ordinary is

Fv=pmt [((1+r/k)^(kn)-1)÷(r/k)]

Fv future value 800000

PMT monthly payment?

R interest rate 0.05

K compounded monthly 12

T time 20 years

Solve the formula for PMT

PMT=Fv÷[((1+r/k)^(kn)-1)÷(r/k)]

PMT=800,000÷(((1+0.05÷12)^(12

×20)−1)÷(0.05÷12))

PMT=1,946.31 per month

Interest earned

800,000−1,946.31×12months×20 years

=332,885.6

Hope it helps!

Answer:

$120,000

Explanation:

Total amount for inclusion in determining Mill Corp's net income or loss is as follows.

- Net loss from disposal of business segment = $100,000

- Property tax for 6 months to June 30, 20x5= $40,000 * 0.5 = $20,000

Therefore, total amount for inclusion = $100,000 + $20,000 = $120,000.

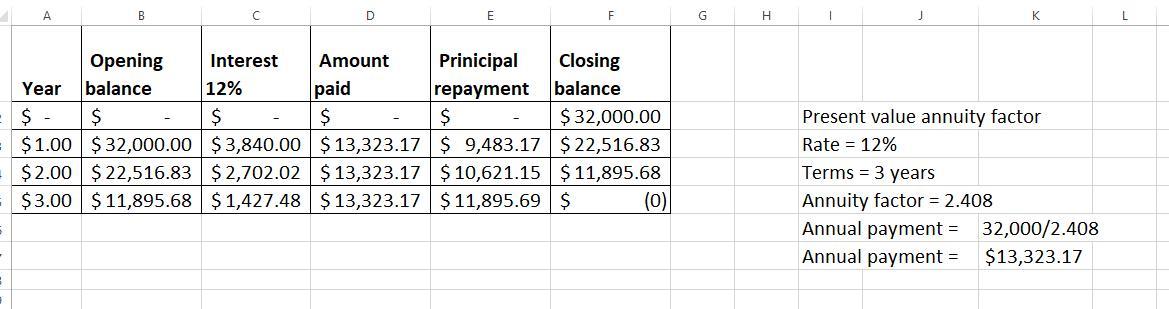

Answer:

Amortization schedule is attached.

Explanation:

Key matrix

Present value annuity factor

Rate = 12%

Terms = 3 years

Annuity factor = 2.408 (this can be derived from present value table - annuity factor)

Annual payment = 32,000/2.408

Annual payment = $13,323.17

Streching, first by raising your arms to while bressthing, and centering yourself to start your yoga moves