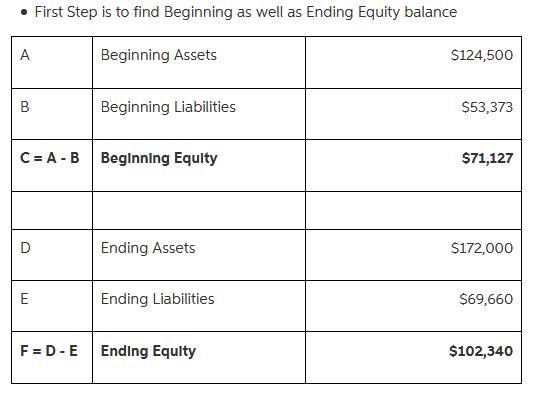

Answer:

Hence, the net income earned or net loss incurred by the business during the year $102,340.

Explanation:

Likely yearly cost based on the above information and no other expenses is $4,800

Answer:

e. by receiving a reward commensurate with their performance.

Explanation:

The word equity means that something is fair. Thus, the equity theory states that employees are motivated when things are fair, and the very definition of fairness in the workplace is receiving a reward that is equivalent to personal performance.

According to this theory, people do not want to earn more than they deserve, they simply want to be compensated accordingly to what they produced.

Answer:

searching products by brand

Explanation:

Generally customers search products by brand or by attributes. When you search products by attributes you are looking for some specific product and you are not that interested about the brand of the product, e.g. you are searching for a dress and your emphasis is towards the design of the dress not the brand. When you search by brand, you assign a different value to each brand that you are searching, depending on which brands you like the most or feel more comfortable with.

In this case, Brenda probably has a very good idea about the products that each brand offers and depending on her clients will decide which brand's products to offer.