Answer:

The correct answer is Voice.

Explanation:

Taking into account the framework of exit, voice, loyalty and negligence, voice means directly raising comments on a particular situation that influences within the work team, so that superiors are aware of situations and can ask themselves solutions for the benefit of all.

Answer:

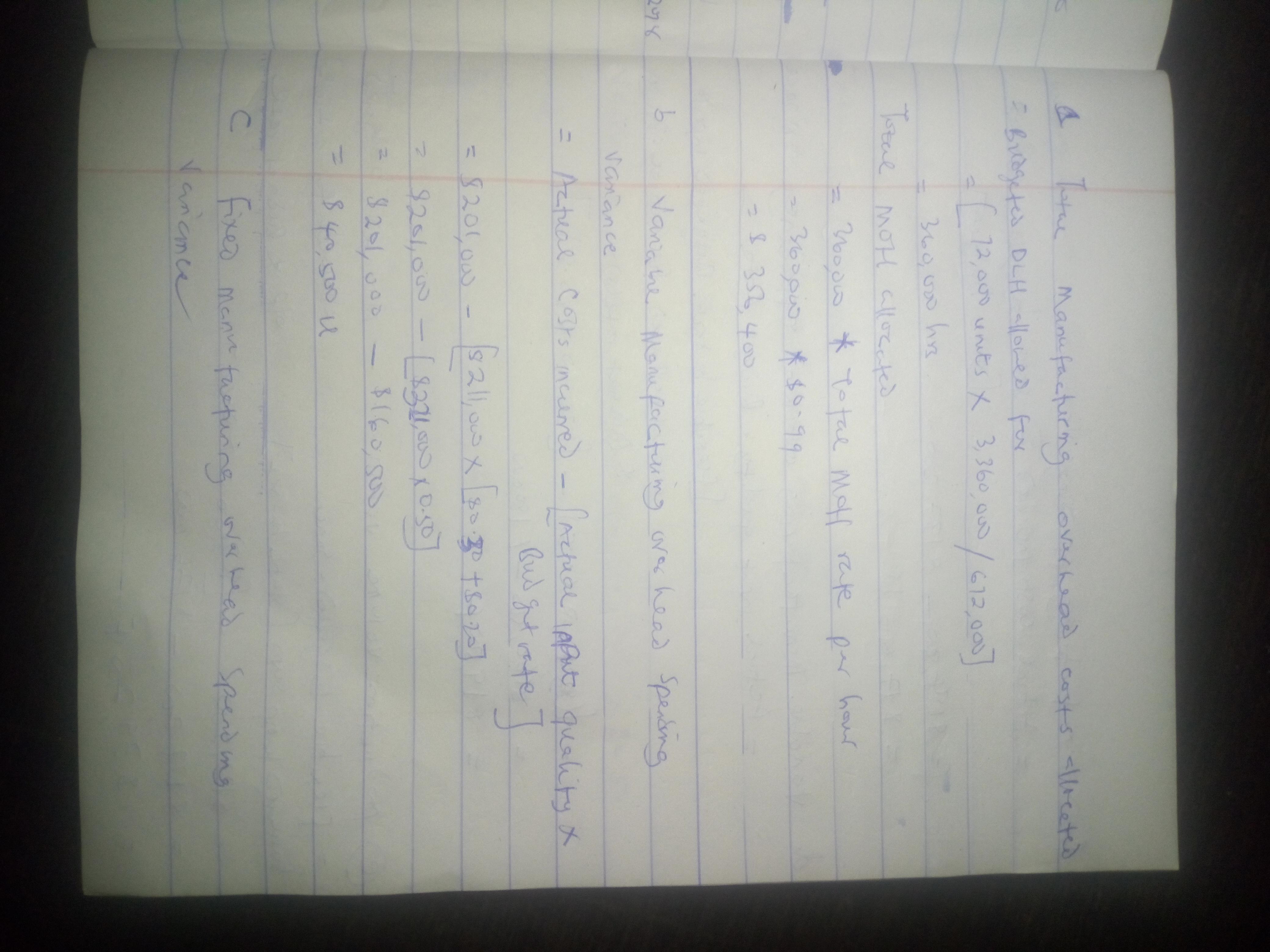

Please see attached solution

Explanation:

a. Total manufacturing overhead costs allocated $356,400

b. Variable manufacturing overhead spending variance $40,500U

c. Fixed manufacturing overhead spending variance $17,600U

d. Variable manufacturing overhead efficiency variance $19,500F

e. Production volume variance $39,200F

Please find attached detailed solution to the above questions

Answer:

$37,000

Explanation:

The computation of the bad debt expense is shown below:

= Amount estimated as uncollectible + written off amount - credit balance of allowance for bad debts

= $28,000 + $15,000 - $6,000

= $37,000

We simply applied the above formula to determine the bad debt expense. Hence, all other information which is given is not relevant therefore, ignored it

Flow to Equity (FTE) is the approach to capital budgeting that discounts the after-tax cash flow from a project going to the equity holders of a levered firm.

An alternative capital budgeting strategy is the flow to equity (FTE) or free cash flow approach. The FTE approach merely requires that equity capital be discounted at the cost of the cash flows from the project to the equity holders of the leveraged firm. The amount of cash that a company's equity shareholders have access to after all costs, reinvestment, and debt repayment is taken into account is known as flow to equity. Free Cash Flow to Equity (FCFE) is calculated as Net Income - (Capital Expenditures - Depreciation) - (Change in Non-cash Working Capital) - (Change in Non-cash Equity) + (New Debt Issued - Debt Repayments) This is the cash flow that can be used to repurchase stock or pay dividends.

More about cash flow brainly.com/question/17406590

#SPJ4

Answer:

The answer is <u>"a. 8.13%".</u>

Explanation:

Given that;

d0 = $1.75

p0 = $40.00

g = 3.6% = 0.036

By using the formula;

Price of the stock = (Dividend this year)(1+g) ÷ (r - g)

By putting the values;

40 = (1.75)(1+0.036) ÷ (r - 0.036)

r - 0.036 = (1.75)(1.036) ÷ 40

r - 0.036 = 1.813 ÷ 40

r - 0.036 = 0.045325

r = 0.045325 + 0.036

r = 0.081325 = 0.081325 x 100

<u>r = 8.13%</u>