Answer:

The correct answer is letter "A": perpetuity.

Explanation:

Annuities are regularly-provided income hired through insurance. Those payments can be provided within a short or long period of time until an undetermined date. That is the reason why annuities are also called perpetuities. Annuities are taxed at regular income tax rates.

Answer:

The correct word for the blank space is: mixed.

Explanation:

Mixed costs or semi-variable costs are the results of adding fixed costs (those that do not change) to a variable cost (vary in proportion to the level of activity). Different levels of production in a company determine how much the mixed cost will be.

Thus, <em>in Jack's case, his salary is the fixed costs and the $1.25 per unit assembled is the variable cost.</em>

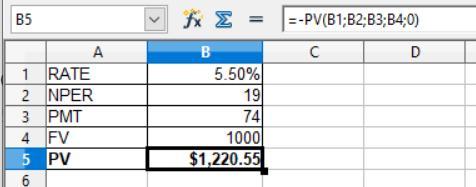

Answer:

$1,220.55

Explanation:

We use the Present value formula to find out the current price of the bonds. The calculation is presented on the excel spreadsheet

Given that,

Future value = $1,000

Rate of interest = 5.5%

NPER = 19 years

PMT = $1,000 × 7.4% = $74

The formula is shown below:

= -PV(Rate,NPER,PMT,FV,type)

So, after solving this, the current price of the bond is $1,220.55

There are various organizations structure. one of it is centralization. <u>Centralization</u> is the degree to which decision-making authority is retained at higher managerial levels.

<h3>Features of Centralization</h3>

In a centralized company, cogent decisions are made at topmost levels of the hierarchy, whereas in decentralized companies, decisions are made and problems are solved at lower levels by employees who are closer to the problem.

<h3>Advantages of centralization</h3>

Some employees are more okay in an organization where their manager authoritatively gives instructions and makes decisions. Centralization can also lead to operational efficiency because there will be no time wasting, particularly if the company is operating in a stable environment. Strategic process and content as mediators between organizational context and structure.

Therefore, the answer is centralization option C.

learn more about centralization: brainly.com/question/1288780

Answer:

c. 12 pairs of jeans per pair of shoes

Explanation:

Suppose that Spain and Germany both produce jeans and shoes.

Spain's opportunity cost of producing a pair of shoes is 5 pairs of jeans Germany's opportunity cost of producing a pair of shoes is 10 pairs of jeans.

By comparing the opportunity cost of producing shoes in the two countries, you can tell that__Spain__ has a comparative advantage in the production of shoes and _Germany__has a comparative advantage in the production of jeans.

Similarly, Germany can gain from trade as long as it receives more than 10 pair of shoes for each pair of jeans it exports to Spain.

Based on your answer to the last question, which of the following terms of trade (that is, price of shoes in terms of jeans) would allow both Germany and Spain to gain from trade?

c. 12 pairs of jeans per pair of shoes