Missing Part of Question:

The question was missing information. Luckily, I found the question on the internet and I am attaching it here for ease of understanding.

<h2>

Answer:</h2>

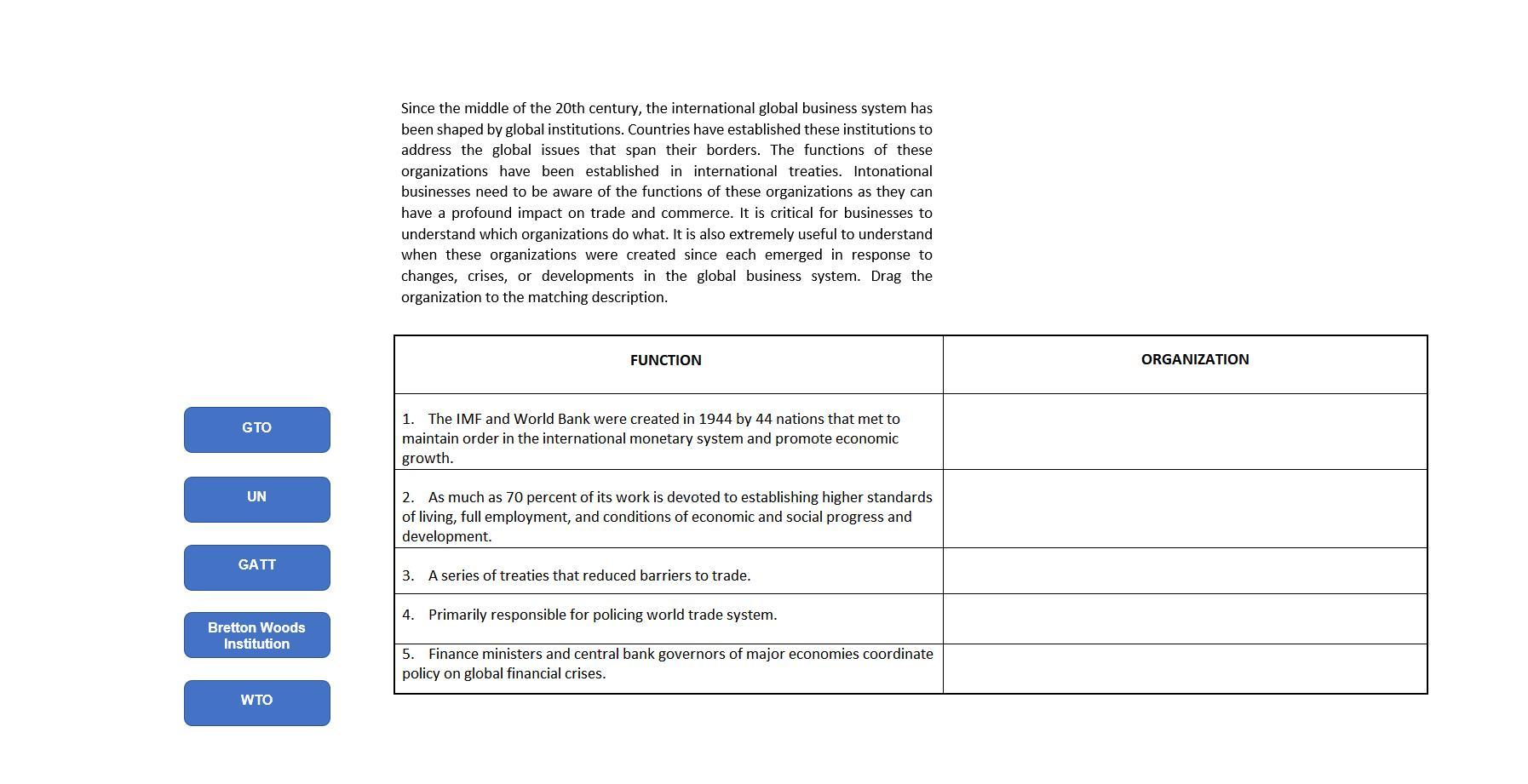

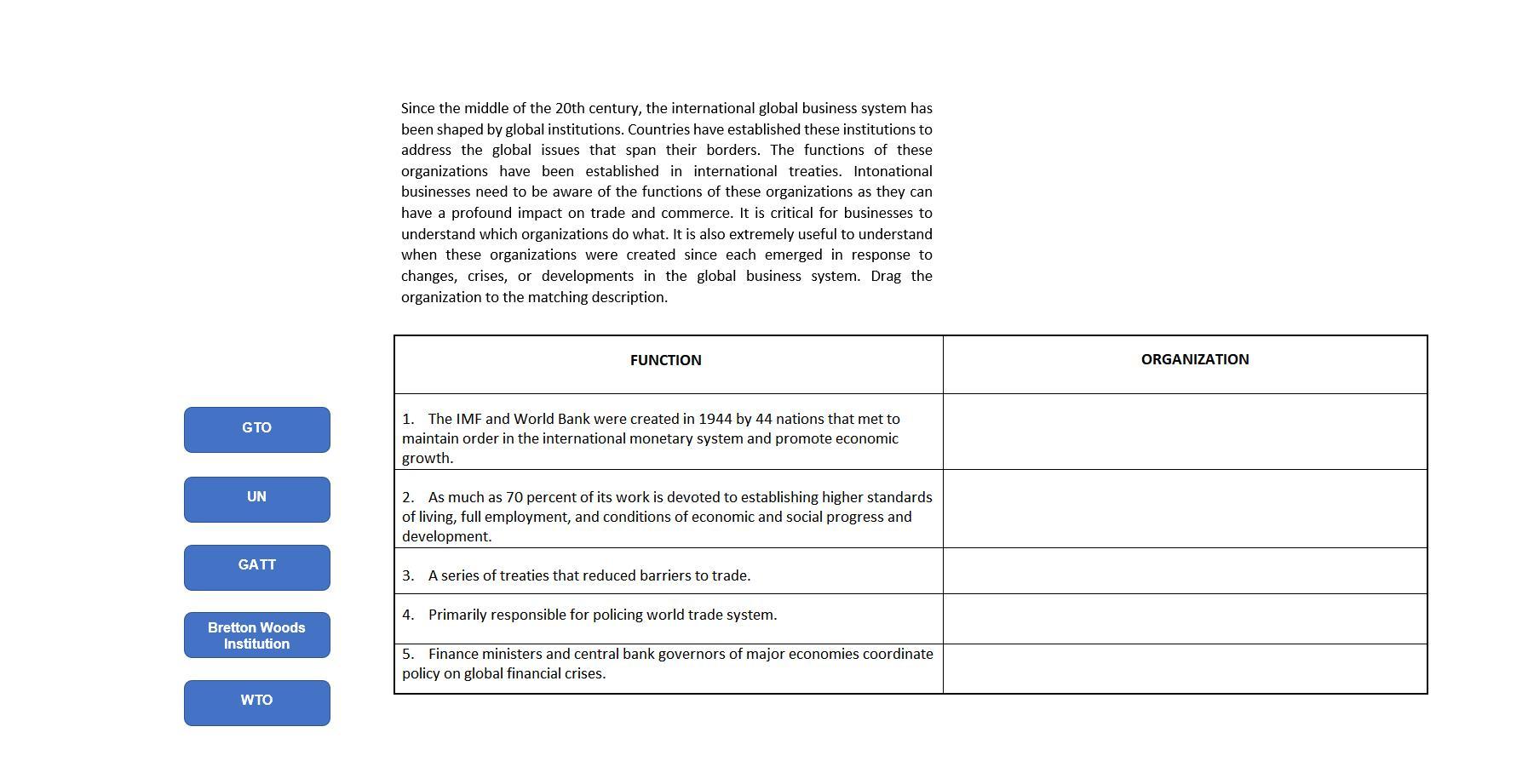

In the order of the functions:

1. Bretton Woods Institutions

2. UN

3. GATT

4. WTO

5. GTO or G20

<h2>

Explanation:</h2>

1. The Bretton Woods Institutions are the World Bank and the International Monetary Fund (IMF).

2. The United Nations is an intergovernmental organization with an objective of maintaining international peace and security.

3. The General Agreement on Tariffs and Trade (GATT) is a treaty between many countries. Its aim is to promote international trade by reducing or eliminating trade barriers like quotas or tariffs.

4. The World Trade Organization is also an intergovernmental organization. Its function is the regulation of international trade among nations.

5. The G20 (i.e. The Group of 20) is an international forum for the governments and central bank governors consisting of 19 countries and the European Union (EU). It focuses on the promotion of international financial stability.