Answer:

C,)The reciprocity norm

Explanation:

From the question, we are informed about Sharon who is upset with her secretary. Though everyone in the office agreed not to give Christmas presents this year, Sharon's secretary gave her an expensive bottle of perfume. In this case, the best yet that identifies the source of Sharon's feelings is reciprocity norm.

Reciprocity norm can be regarded as rule of human interaction which stressed that action of a person needs to be reciprocated by another people. In simple term, reciprocity norm explain that when a particular person is been given a gift by another, the gift must be related by the person, this gift could take different number of forms. Reciprocity can be explained better as ways and how particular positive actions generate more positive actions, in the same way that negative actions generate or give room for more negative actions

Total output of an economy can be divided into its alternative uses by considering who bought the output. when other countries purchase part of an economy's output, this is called Gross Domestic Product [GDP],

<h3>Gross Domestic Product</h3>

The total monetary or market worth of all the finished goods and services produced within a nation's boundaries during a certain time period is known as the gross domestic product (GDP). It serves as a thorough assessment of the state of the economy in a particular nation because it is a wide indicator of total domestic production.

Although it is often calculated on a yearly basis, GDP can also be computed on a quarterly basis. For instance, the US government estimates the annualized GDP for the entire year as well as each fiscal quarter.

To know more about 'GDP', visit :brainly.com/question/1383956

#SPJ4

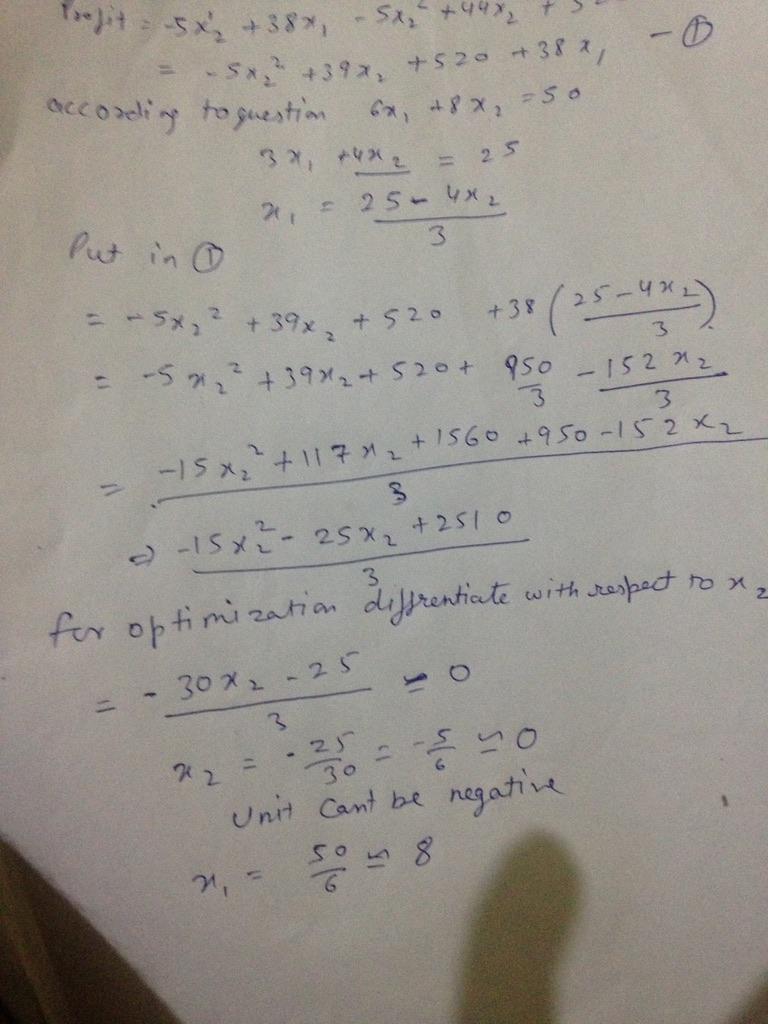

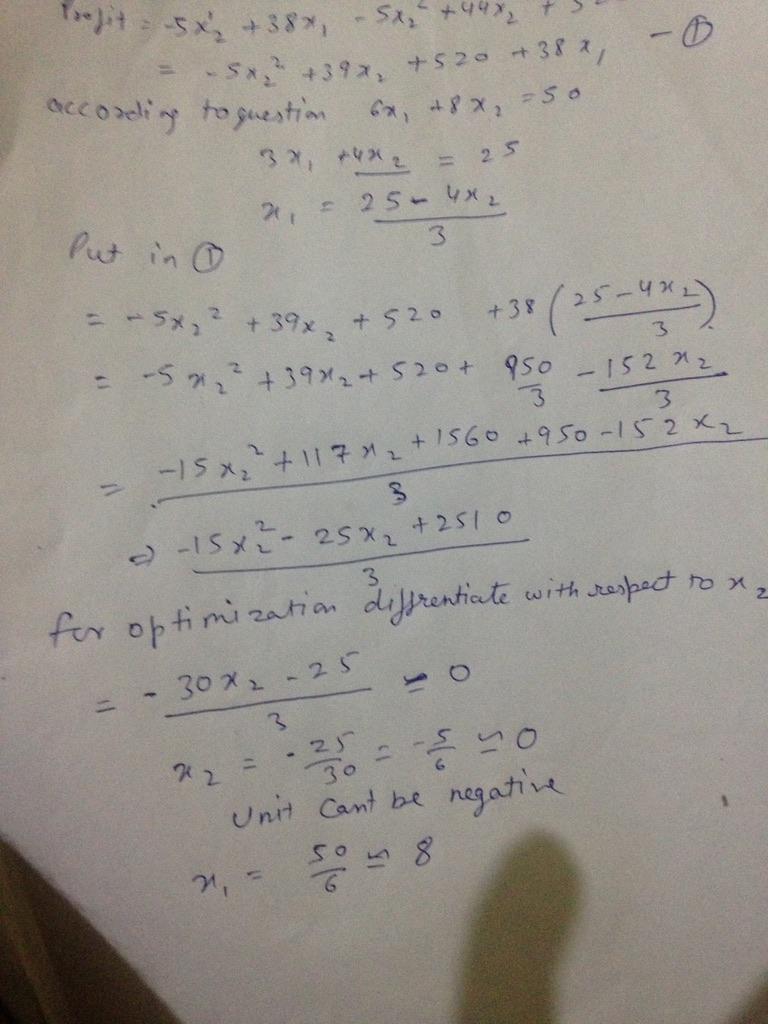

Answer

The answer and procedures of the exercise are attached in the following archives.

Explanation

You will find the procedures, formulas or necessary explanations in the archive attached below. If you have any question ask and I will aclare your doubts kindly.

Answer:

False

Explanation:

Angel Investors are investors who invest in new start-ups in order to help them get moving and be able to advance with their goals and visions for the business. They do this in exchange for an ownership equity of the startup that they are investing in. This being the case, since Ted wants to exercise sole ownership and control over the firm for as long as possible, it can be said that it will not be easy to find Angel investors willing to help him meet his financial needs.

I hope this answered your question. If you have any more questions feel free to ask away at Brainly.

<span>Scientists and mathematicians would be greatly beneficial to the project due to their ability to help us calculate our cost and effect on the environment, as well as maximize our budget with their calculations. I hope you all realize how important these new additions to our team are.</span>