Answer:

The price of this car=$13,015.925

Explanation:

Given data:

Amount each year=$2,500

Time period=7 years

interest rate=8%

Required:

The price of this car=?

Solution:

The Formula we are going to use is:

Where:

PV is the price of car i.e present value

A is the payment made each year

n is the time period in which payments are paid

r is the interest rate

A=$2,500, r=8%=0.08, n=7

The price of this car=$13,015.925

Answer: False

Explanation: The reason is that Retained earning are considered as opportunity cost. Because retained earnings could be used to distribute profit among shareholders and they could invest somewhere to get return. Or retained earnings could be retained by the firm to invest in the company activities itself.

Incomplete question. The options read:

a. 5.16

b. 5.35

c. 5.56

d. 5.77

e. 5.99

Answer:

<u>b. 5.35</u>

Explanation:

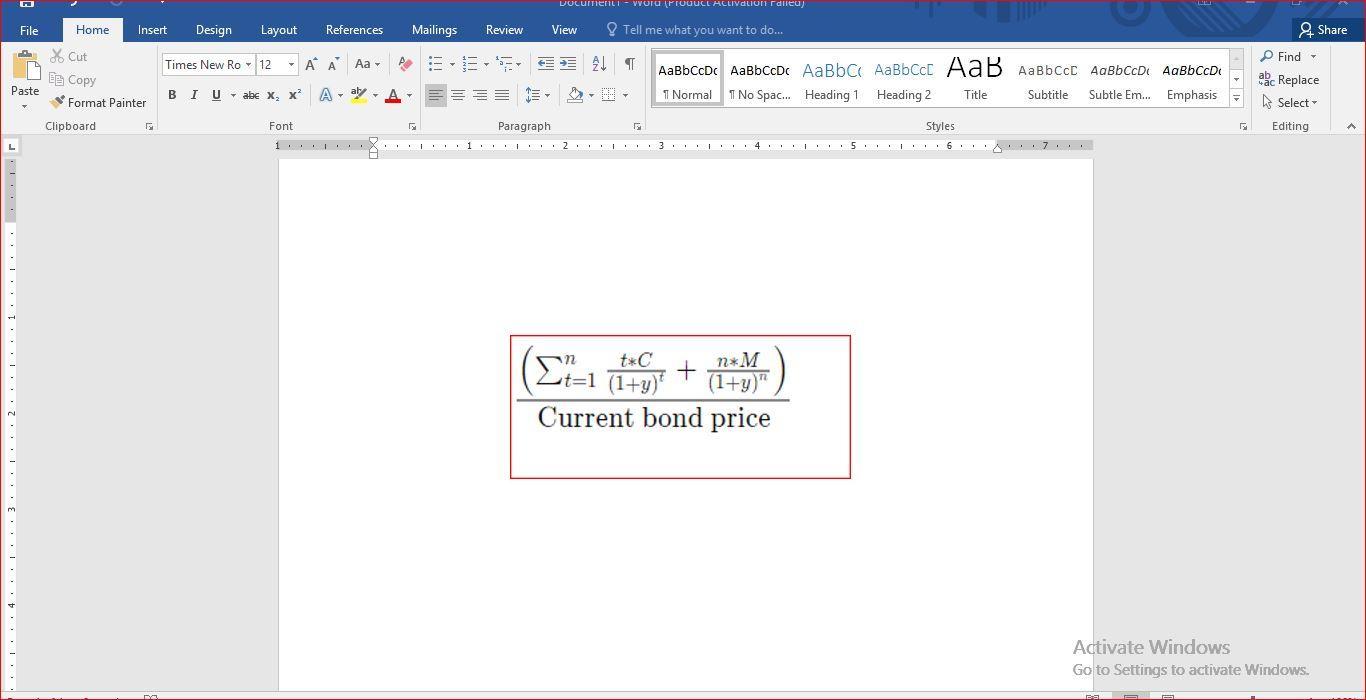

Remember, we use the Macaulay duration to determine the weighted average time before any bondholder would start to receive their expected bond's cash flows.

Hence, using the formula attached below, we could find the Macaulay duration for this scenario. In the above formula, where:

C= the periodic coupon payment

y= the periodic yield

M= the bond’s maturity value

n= duration of bond in periods.

However, another way to get a solution is to employ an advanced calculator.

Answer: $32,667

Explanation:

The truck's useful life is 3 years because it is 2007 to 2010.

Depreciation = (Cost - Salvage value) / Useful life

= (110,000 - 12,000) / 3

= $32,667 per year