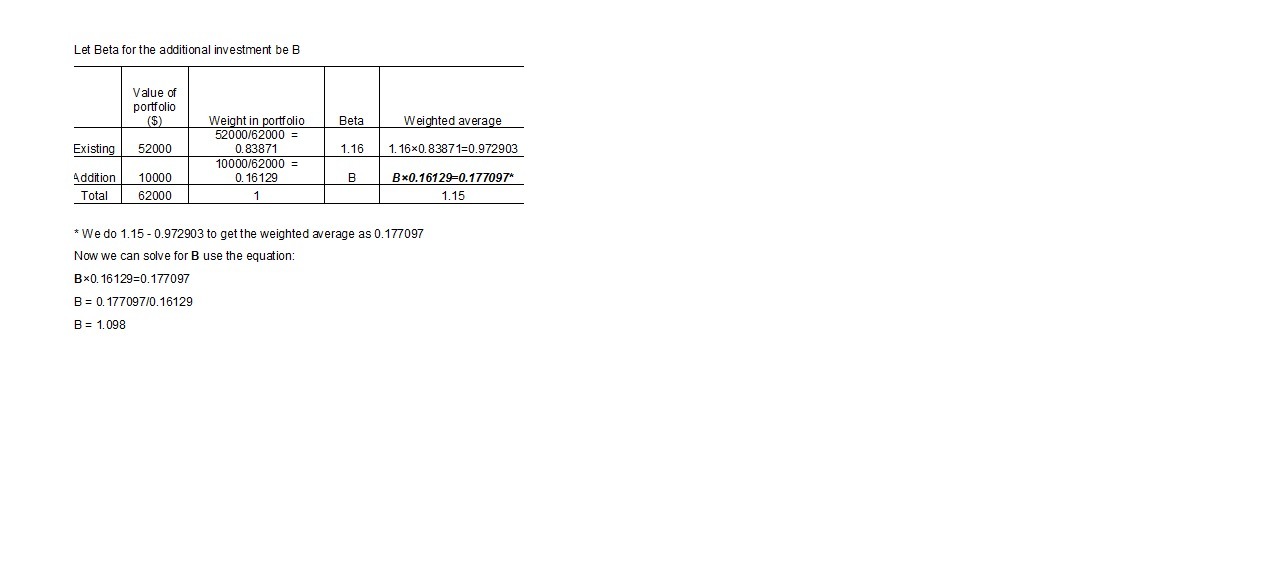

The beta of the new investment must be 1.098.

We need to use the concept of weighted averages to solve this problem.

We find the ratios of the dollar value of existing to the total new portfolio and additional investments to the total new portfolio and find the weights.

We then find the product of the beta of the existing portfolio and its respective weight calculated in the earlier step, with the given data.

We derive the product of the additional investment and beta by subtracting the answer from the earlier step from the new portfolio's beta (1.15).

Then we work backwards to arrive at the the beta for the additional investment.

Answer:

Hedge funds

Explanation:

A mortgage is a long-term loan facility used to finance the purchase of homes and other properties. It is a long-term loan due to the high amount that needs to be borrowed. Customers in need of a mortgage facility may go to a bank, mortgage bankers, or savings and loan institution.

A hedge fund is a portfolio investment instrument. It is an association between a professional fund manager and investors. They pool their resources together in diversified investments. The investors are passive while the fund manager aggressively invests the funds r to generate higher returns to the investors.

Answer:

She consumes 41 units of good X.

Explanation:

Utility Maximization:

The maximum utility that a consumer derives from the use of a specified amount of a good or service.

Consumer M

aximise the utility when following condition is satisfied.

MUx / MUy = Px / Py

Y / X = 5 / 4

4Y = 5X

According to given sitation the budget constraint is

Px ( X ) + Py ( Y )= M

5X + 4Y = 410

Using 4Y = 5X

thus, 5X + 4Y = 410

5X + 5X = 410

10X = $410

X = 41.

There are many developments which occured in recent years as with the changing technology, shape of products and techologie has changed plenty and there is the special fashion which affects emplyoees stress and additionally management stress.

Re-engineering approach restructuring the product at huge range and it contributed to employees stress as the employee has understood the exclusive merchandise shape over and over by way of having the training to increase their goodwill as an employee in the marketplace and also to meet competitions. Also, it contributed to management pressure with the aid of having high competition among organizations regarding this.

Reorganizing ways changed the way of the method and once more it contributed to emplyoee strain and control stress to fulfill the excessive degree competitom with the aid of updating their corporations with new and contemporary technology.

Formation of health machine has a high-quality impact on each emplyoee as well as management because it helps emplyoee for being healthful and control to have extra healthy emplyoees.

Learn more about stress here brainly.com/question/26108464

#SPJ4

Ummm well it depending on the person who is forcing you to sign it or making you do it like for example like the tease you saying that if you sign it i will give you 1million dollars but after that you want your money back etc. and they said its too late cause you all already sign it and then you gonna go to court or the police or a lawyer for that.