Answer:

Answer for the question:

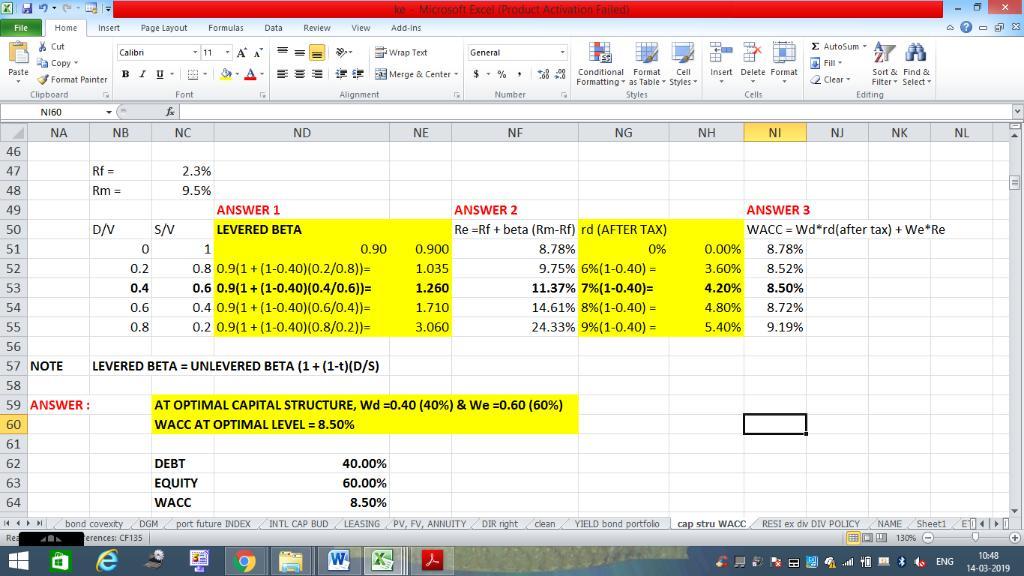

Consider Optitron Enterprises, a firm that is currently funded entirely with equity. There are 50 million shares outstanding and each share has a current market value of $15. Eric Fredrickson, the CEO, has considered whether the company should take on some debt, as he has learned in his Executive MBA class that some debt can increase shareholder value. Mr. Fredrickson has estimated that the current risk free rate is 1.9% and the expected return on a broad market portfolio is 9%. The company’s marginal tax rate is 40% and its operating beta (also known as unlevered beta) is 0.75. Mr. Fredrickson has contacted an investment banker who has analyzed the firm’s operational risk and financial condition. The investment banker has provided the following schedule of anticipated debt costs at various levels of debt financing. Optitron would use any proceeds from a debt issue to immediately retire outstanding equity by repurchasing shares, also known as a recapitalization. wd rd 0 0.0% 0.20 6.5% 0.40 7.5% 0.60 8.5% 0.80 9.5% 1. Using the Hamada equation, estimate the firm’s beta at each level of debt. 2. Using the CAPM, estimate the firm’s cost of equity at each level of debt.

is given in the attachment.

Explanation:

Conscientious employees prioritize <u>accomplishment</u> striving, indicating a strong desire to achieve task-related goals as a means of expressing their personality.

<h3>What is meant by Conscientious employees ?</h3>

This is the term that is sued to refer to the types of workers that are in an establishment who are willing to work like they are supposed to. These are the people that would do the right thing and are described to have a near perfect personality in the work place.

Hence we can say that Conscientious employees prioritize accomplishment striving, indicating a strong desire to achieve task-related goals as a means of expressing their personality.

Read more on conscientiousness here: brainly.com/question/11372064

#SPJ1

Answer:

The correct answer is option (b) The present value of the lease payments less the present value of the guaranteed residual value (if any)

Explanation:

For balance sheet, the liability of lease is measured as the present value of lease payments less the present value of the guaranteed residual value.

Normally, the equipment been leased by the company will record the equipment as an asset, and a liability will be recognize by the company on the balance sheet, by an amount identical to the present value of the lease minimum payments lease residual value guaranteed, if there are any.

Answer:

There is no specific type of contract to define this agreement, as it was a verbal acceptance. And yes, there is a difference in the use of cellphone and voicemail as there would be a time difference. Please give brainliest.

True, E-mail is usually considered as a formal mode of communication.

<u>Explanation:</u>

A formal mode of communication is when the information is transferred from a pre defined channel, from a top level management to the lower level of the employees.

It is considered formal because of the specific word limit that a email can carry and it is in written form. Any kind of information when conveyed in written form is considered formal because it holds authenticity. Therefore, mail is the best mode.