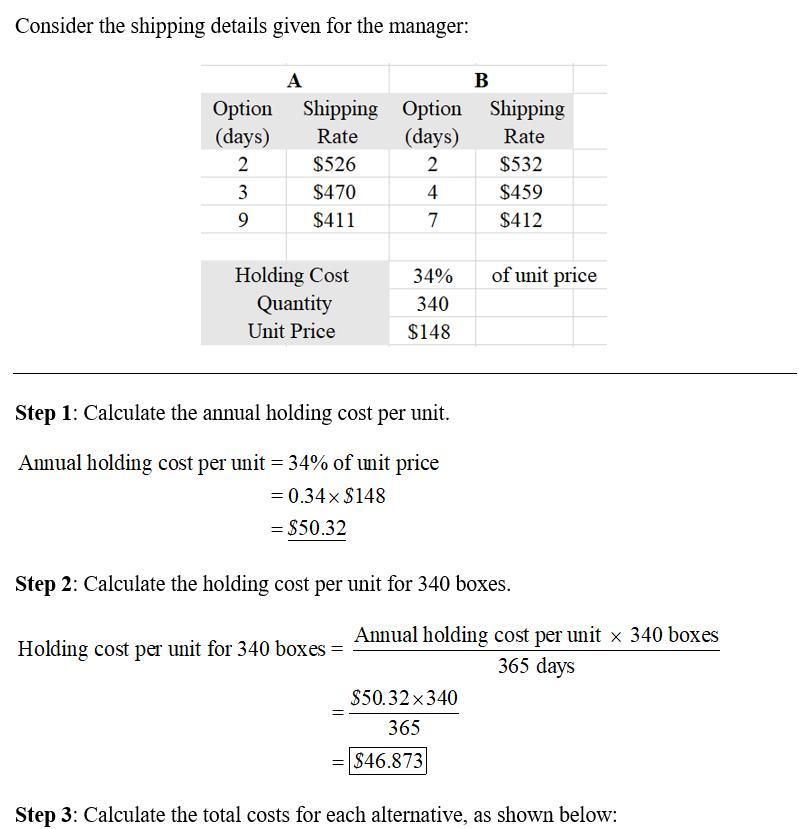

Answer:

(1) the double-declining-balance method

Depreciation for 2018 = $16,000

Depreciation for 2019 = $9,600

Book value of the spooler at December 31, 2018 = $24,000

Book value of the spooler at December 31, 2019 = $14,400

(2) the sum-of-year digits

Depreciation for 2018 = $12,000

Depreciation for 2019 = $9,600

Book value of the spooler at December 31, 2018 = $28,000

Book value of the spooler at December 31, 2019 = $18,400

Explanation:

(1) the double-declining-balance method

Note: See part 1 of the attached excel file for the computation of depreciation for 2018 and 2019 and the book value of the spooler at December 31, 2018 and 2019 using the double-declining-balance method.

Double-declining-balance method can be described as a depreciation technique in which the rate at which an asset is depreciated is twice depreciation rate for the straight line depreciation method.

The double-declining-balance depreciation rate for Morrow Inc. can therefore be calculated as follows:

Straight line depreciation rate = 1 / Number of expected useful years = 1 / 5 = 0.20, or 20%

Double-declining depreciation rate = Straight line depreciation rate * 2 = 20% * 2 = 40%

The 40% double-declining depreciation rate is what is employed in part 1 of the attached excel file table.

Note:

Although this is not part of the question but it will be useful for you in the future. The depreciation expenses for year 2022 is calculated by deducting the residual value of $4,000 from the 2022 Beginning depreciable amount (i.e. $5,184 - $4,000 = $1,184). The residual value of $4,000 therefore represents the book value at the end of year 2022.

(2) the sum-of-year digits

Note: See part 2 of the attached excel file for the computation of depreciation for 2018 and 2019 and the book value of the spooler at December 31, 2018 and 2019 using the sum-of-year digits method.

The sum-of-year digits method can be described as a depreciation method that accelerates deprecation by assuming that an asset’s productivity falls with the passage of time.

Under the sum-of-year digits method, the remaining useful life of the asset at the beginning of the period is divided by the sum of the year's digits to obtain the deprecation rate for that period.

For this question, the Sum of year digits used in the attached excel file is calculated as follows:

SYD = Sum of year digits = 1 + 2 + 3 + 4 + 5 = 15