Answer:

Explanation:

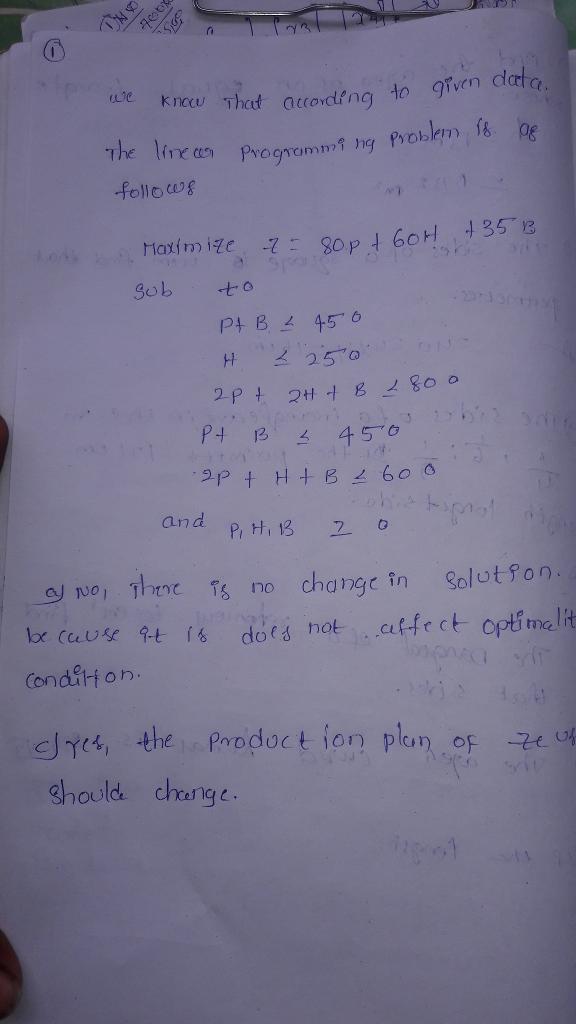

Please check the attached file below to see answer to the given question

Russia, Iran, Japan, South Korea, Mexico, Brazil, Arabia and Belgium

Answer:

c)

Explanation:

Based on the information provided within the question it can be said that this worry stems from the concern that TV networks could be charged with deception of the public by failing to disclose the details of product-placement deals. This is due to the fact that if the network does not tell the public the details of the product deals or even that they are being sponsored, then a consumer might buy the product under the impression that it is a good product when in fact, the network is up-selling it. Therefore it is a form of false advertising.

Answer:

C. Understand that the opportunity cost of attending college is very high.

Explanation:

The reason is that the colleges costs very high both the money and time. However the person can also earn while pursuing their dreams because it has greater value for them if they have potential for growth in games. So they prefer to follow their dreams rather investing on their higher education.

Provide buyers superior value relative to the offerings of rival sellers in order to attain a competitive advantage.

<h3><u>

Explanation:</u></h3>

The strategy or the plan that is being used by a company in a long term for the purpose of gaining advantage over the competitors of the similar field refers to the Competitive Strategy. The main aim of using competitive advantage in the creation of a defensive position so that the competitors will not compete with the company and also aims in attaining higher return on investment.

The types of competitive strategies are differentiation strategies,focus strategies and Cost-leadership strategies. Thus competitive strategies aims in providing superior value to the offerings given to the buyers and gaining a competitive advantage.