Psychological pricing uses price points to designate prices that help make the impression that the product exists less expensive than it is.

<h3>What is Psychological pricing?</h3>

Pricing, which can be a part of a company's marketing strategy, is the process by which a company determines the price at which it will offer its goods and services. Pricing is the process of determining the value that a manufacturer will receive in exchange for their goods and services. The producer uses a pricing strategy to make the cost of its products suitable for both the manufacturer and the consumer.

The use of pricing to sway a customer's purchasing decisions or spending patterns is known as psychological pricing. The objective is to satisfy a customer's psychological need, whether that need is to save money, invest in the best product, or receive a "good deal." A pricing and marketing technique known as psychological pricing is based on the idea that specific prices have psychological effects.

Hence, Psychological pricing uses price points to designate prices that help make the impression that the product exists less expensive than it is.

To learn more about Psychological pricing refer to:

brainly.com/question/7464326

#SPJ4

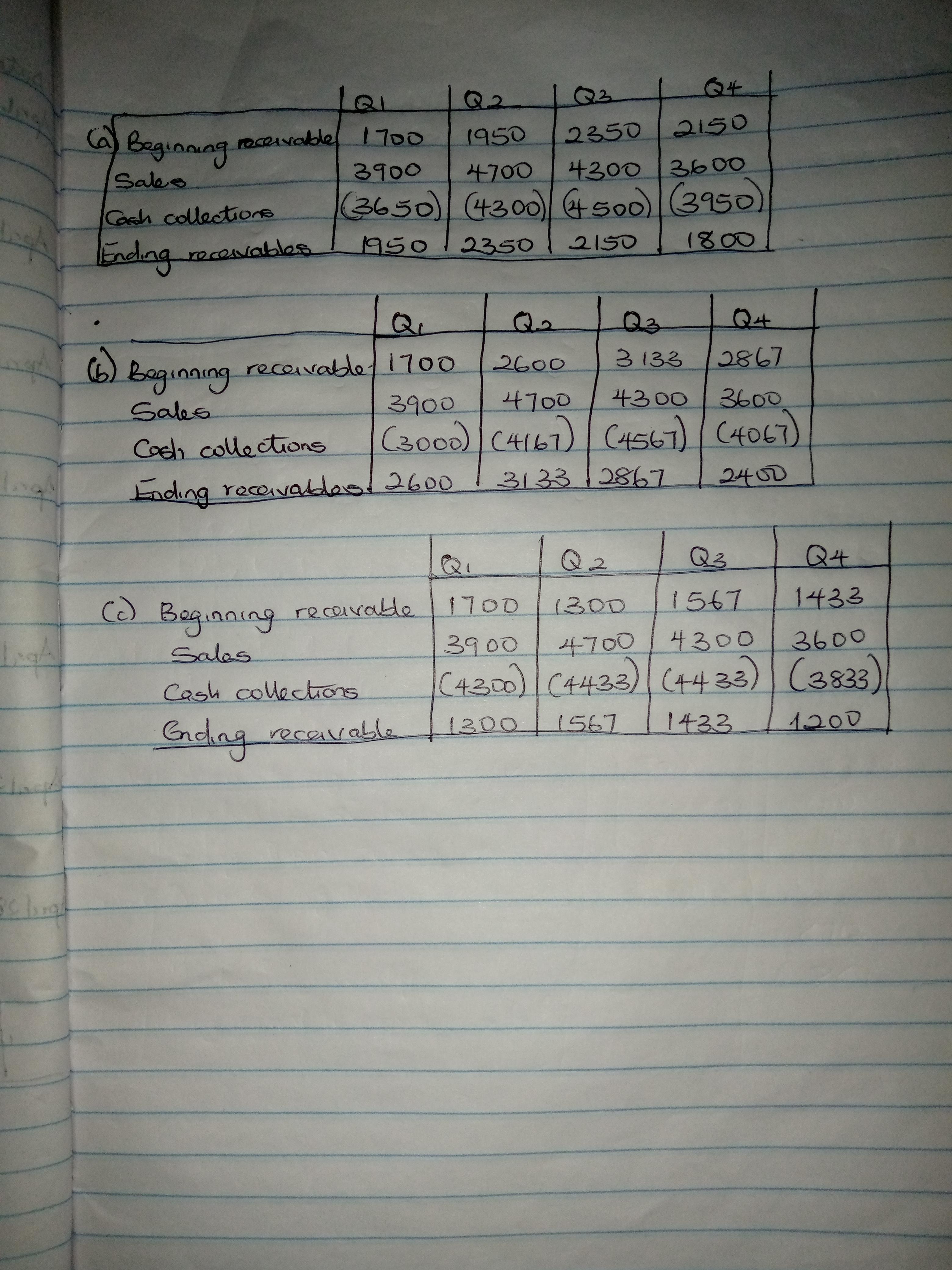

Answer: Check attachment

Explanation:

The cash collection was calculated as:

a. (90-45)/90 = 1/2

Q1 = 1700 + (1/2 × 3900)

= 1700 + 1950

= 3650

Q2 = 1950 + (1/2 × 4700)

= 1950 + 2350

= 4300

Q3 = 2350 + (1/2 × 4300)

= 2350 + 2150

= 4500

Q4 = 2150 + (1/2 × 3600)

= 2150 + 1800

= 3950

Check the attachments for further information.

Answer:

decrease in cell phone supply.

Explanation:

Based on the information provided within the question it can be said that the most likely scenario to arise from this would be the decrease in cell phone supply. This is because an increase in wages means the company needs to make more profit in order to pay for those wages. Therefore they will increase cell phone prices which will most likely cause a decrease in sales which ultimately leads to a decrease in supply otherwise stock would overflow.

I hope this answered your question. If you have any more questions feel free to ask away at Brainly.

Answer:

The correct answer is A) The higher the annual income, the more people get a sense of identity from their job.

Explanation:

Employees do not perceive their duties in the same way when they do so for a lower salary than they aspire to. This situation also affects motivation because they find as if they were giving away their time in exchange for a salary below normal.

Answer:

$230.02

Explanation:

Calculation for what amount would the company have to charge for the Tijerina wedding cake to just break even

Size related $69.16

($1.33 per guest × 52 guests)

Complexity-related $56.84

($28.42 per tier × 2 tiers)

Order-related $74.72

($74.92 per order × 1 order)

Cost of purchased decorations for cake $29.30

Total cost $230.02

($69.16+$56.84+$74.72+$29.30)

The amount that the company would have to charge for the Tijerina wedding cake to just break even will be $230.02