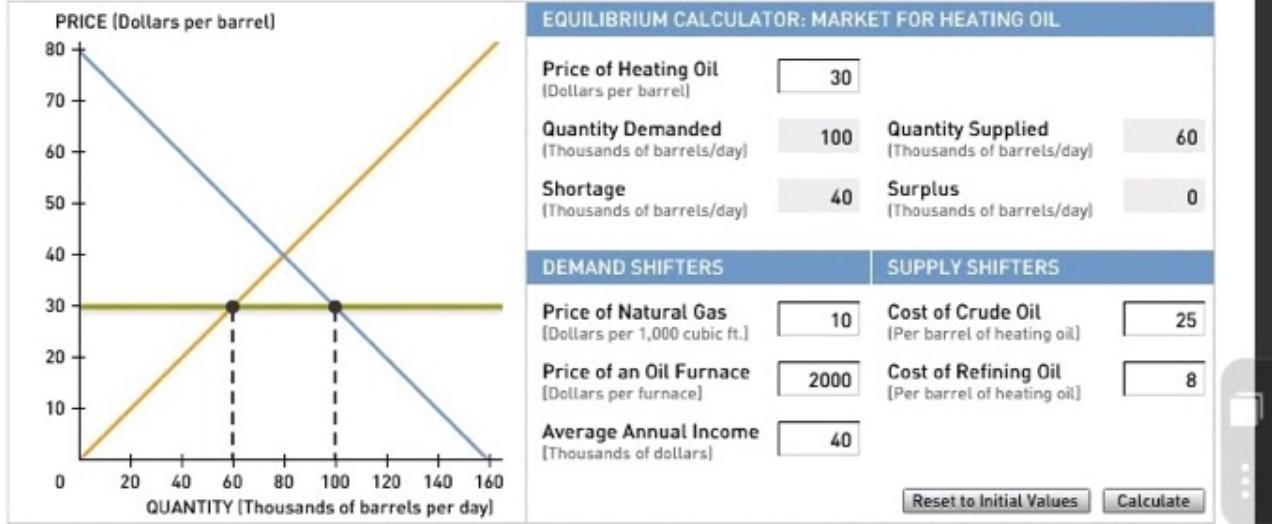

Answer:

1. 80,000

2. $40 per barrel

Explanation:

1. As we can see from the table provided The equilibrium quantity in this market is 80,000 barrels of heating oil per day, as quantity demanded match quantity supplied

2. As we can see from the table provided The equilibrium price is $40 per barrel as in this cost there is an intersection of quantity demanded and quantity supplied. In other words the equilibrium price and quantity could be find out when the quantity demanded equal to quantity supplied

Answer:

A hyper-social knowledge management.

Explanation:

Hyper-social knowledge platforms apply the concepts of social media to information databases. So employees could comment, share, and add to post with important information that they know to help out employees who don't know as much about that subject.

Answer:

True

Explanation:

<em>Absorption costing is a method of costing where production units and inventories are value at the full cost per unit. Here, fixed overheads are charged to all units produced using an overhead absorption rat</em>

<em>Under the traditional absorption costing system, overhead is assigned to units produced using different bases ranging from labour hours, machine hours, e.t.c</em>

Overhead absorption rate = Estimated overhead/Estimated Activity level

Answer : True

Answer:

B. The Sherman Act allows the US government to regulate activities that restrain competition and trade

Explanation:

The Sherman Antitrust Act of 1890 was first legislation enacted by US congress. It was brought into force to regulate competition and trade among enterprises. This act prohibits agreement in restraint of trade or interference of power in trade like price fixing, bid rigging, etc.

The Sherman Act did not work for long as it restrict the business merger and people are confused about knowing the motive of the act as it is not designed properly.