Answer:

Yield to call i.e 6.48%

Explanation:

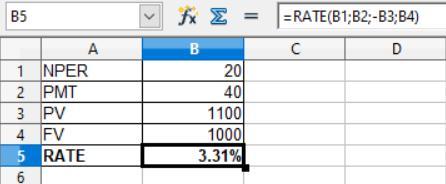

In this question we use the rate formula which is shown in the attachment below:

So in the first case

Given that,

Present value = $1,100

Future value or Face value = $1,000

PMT = 1,000 × 8% ÷ 2 = $40

NPER = 10 years × 2 = 20 years

The formula is shown below:

= Rate(NPER;PMT;-PV;FV;type)

The present value come in negative

So, after solving this, the yield to maturity is 3.31% × 2 = 6.62%

So in the second case

Given that,

Present value = $1,050

Future value or Face value = $1,000

PMT = 1,000 × 8% ÷ 2 = $40

NPER = 5 years × 2 = 10 years

The formula is shown below:

= Rate(NPER;PMT;-PV;FV;type)

The present value come in negative

So, after solving this, the yield to call is 3.24% × 2 = 6.48%

Since yield to call is less than the yield to maturity so the yield to call is to be earned