Answer:

c. Increase of $192,500

Explanation:

Note: The full question is attached

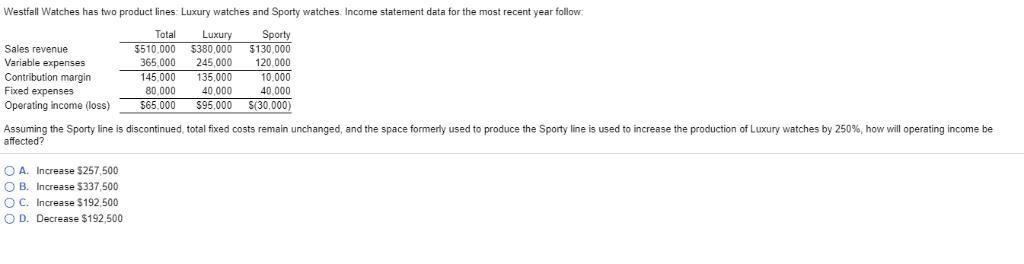

Particulars Luxury Amount$

Sales $950,000

(380000*250/100)

Less: Variable cost $612,500

(245000*250/100

) <u> </u>

Total contribution $337,500

Less: Fixed expenses <u>$80,000 </u>

Net Operating Income <u>$257,500</u>

Change in Operating Income = New Profit - Existing profit = $257,500 - $65,000 = $192,500

Hence, there is an increase of $192,500