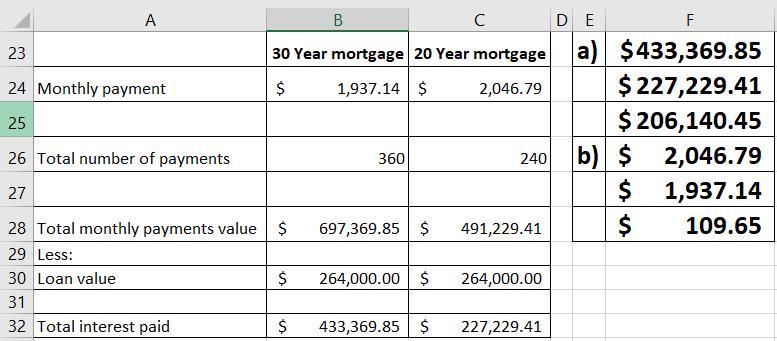

C, because debtors like having narrower debts.

Answer:

Explanation:

COMMUNITY, FAMILY, & PERSONAL SERVICES.A program that focuses on the development and implementation of public, private, and voluntary support services for individuals, families, and localities and that prepares individuals to function in a variety of occupations promoting family life, and family/community development.

AGRICULTURE & NATURAL RESOURCES CONSERVATION.Conservation in agriculture is vital to maintain the productivity and sustainability of America's working and non-working lands. USDA wants to help you improve and preserve your natural resources which can in turn positively impact the profitability of your operation.

Music, Theory & Composition.The study of music theory and composition will also improve your skills as a performing musician. Students of music theory and composition learn how music is put together and what makes it pleasing to the ear. Classes cover such topics as melody, harmony, form, improvisation, and computer skills.

i cant write anymore it wont let me

Answer: Option B

Explanation: Foreign direct investment can be defined as a situation in which a company invest in a country other than its home country. In such a case, the company starts a new setup in the new country with the same business operation.

For example an automobile company of Germany opening their car showrooms in america.

Thus, from the above we can conclude that the correct option is B.

Answer:

D. how much the person has borrowed compared to how much he or she earns

Explanation:

A person's debt-to-income ratio, abbreviated as DTI, is a measure of a person's monthly debt obligation against their monthly gross income. It shows the fraction or percentage of gross income that is committed to debt repayments. Lenders use the debt-to-income ratio to assess a borrower's ability to repay future loans.

Calculating the debt-to-income ratio requires one to add up all their existing loan repayments and divide that figure with their gross income. Lenders insist on a ration that does not exceed 36% as per the 28/36 rule.