When a firm can depreciate its capital equipment over a shorter period, it cuts its taxes now.

A capital asset's value dropping is referred to as capital depreciation. To determine the recovery cost incurred on fixed assets over the course of their useful lives, assets are depreciated. When the asset reaches the end of its useful life or you need to sell it, this is used as a sinking fund to replace it. Depreciation lowers the taxable income, which lowers the tax burden. Capital assets are listed as an asset on the balance sheet and are depreciated over the course of their useful lives. Businesses typically have to spread out the costs of capital investments over a number of years in accordance with predetermined depreciation schedules.

More about depreciation brainly.com/question/15178885

#SPJ4

Answer:

i think commercial banks aren't

Answer:

total variable cost increases

Explanation:

Variable cost refers to the expenses that change with production volume. There is a direct relationship between variable costs and the level of production. An increase in the output level will result in a rise in variable costs. For sales volume to increase, the output level must have been high.

A high production level is necessary to support a high sales volume. Examples of variable costs are packaging and raw materials. A high output level will require the use of a large volume of raw materials, hence higher costs. Fixed cost contrast variable costs, as they do not change with varying output.

Answer:

marginal cost = $2

Explanation:

given data:

cost on wool when 10 sweater made in one month = $15

cost on wool when 11 sweater made in one month = $17

fixed cost = $100

In case of no other cost present, marginal cost is given by

Marginal cost = cost of eleven sweaters - cost of ten sweaters

= $17 -$15

= $2

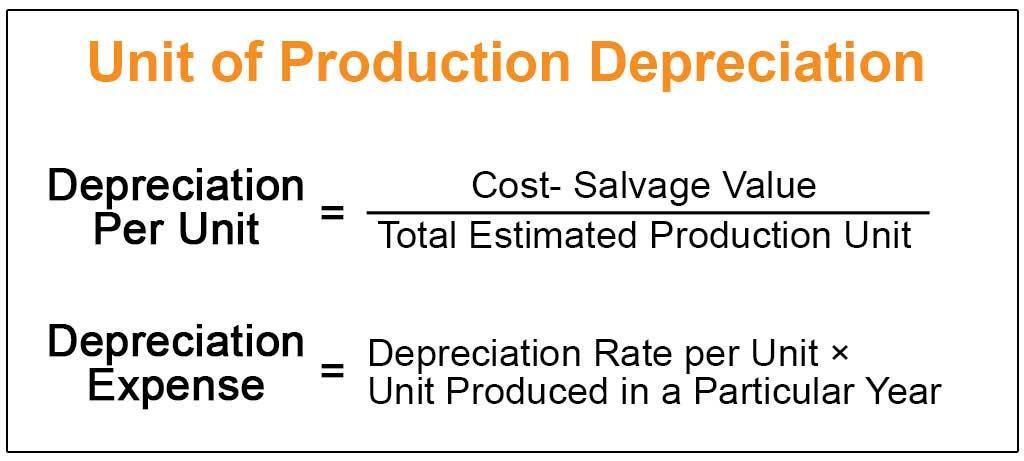

Answer:

<u>Depreciation expense per year</u>

Year 1 = $1200

Year 2 = $800

Year 3 = $600

Year 4 = $300

Year 5 = $100

Explanation:

To determine the depreciation expense under the units of production/activity method of charging depreciation, we will first calculate the depreciation expense per unit and then multiply it with the units of production in each year to calculate the depreciation expense for that year.

The formula for depreciation under this method is attached.

Depreciation per unit = (3000 - 0) / 30000 = $0.1 per copy

<u />

<u>Depreciation expense per year</u>

Year 1 = 0.1 * 12000 = $1200

Year 2 = 0.1 * 8000 = $800

Year 3 = 0.1 * 6000 = $600

Year 4 = 0.1 * 3000 = $300

Year 5 = 0.1 * 1000 = $100