A large assortment of each item within a product line in a store is referred to as breadth of the product line.

Product width, also called width, is the number of product lines offered by a company. For example, a shoe store's width would be 6 if it had Nike in stock. Asics.

Product Width indicates the number of different products the store sells. The more products offered, the wider the product range of this company. Product depth indicates how many variations of each product a store carries.

The number of products in a product line is related to the depth of the product line, and the number of individual product lines within the enterprise is the width (or breadth) of the product line.

Learn more about product line here: brainly.com/question/15187131

#SPJ4

Answer:

both

- United Continental with a capital expenditure of 60.68%

- Southwest Airlines with a capital expenditure of 51.38%

Explanation:

Since United Continental's purchases of Boeing planes represent over 60% of their capital expenditures, this means that Boeing had to be the primary plane supplier. Even if the company purchased planes form other manufacturer, their purchases would not even be 40% of the company's purchases.

The same applies to Southwest Airlines, even though the purchases from Boeing are a little lower, they are still over 51%. This means the company could not have spent more money on purchasing planes from another company. The maximum purchase from another airplane manufacturer would have been less than 49% at most.

Besides the previous analysis, you must also consider that the company spends money on things besides airplanes, e.g. new training facilities, equipment, computer software, other vehicles, etc.

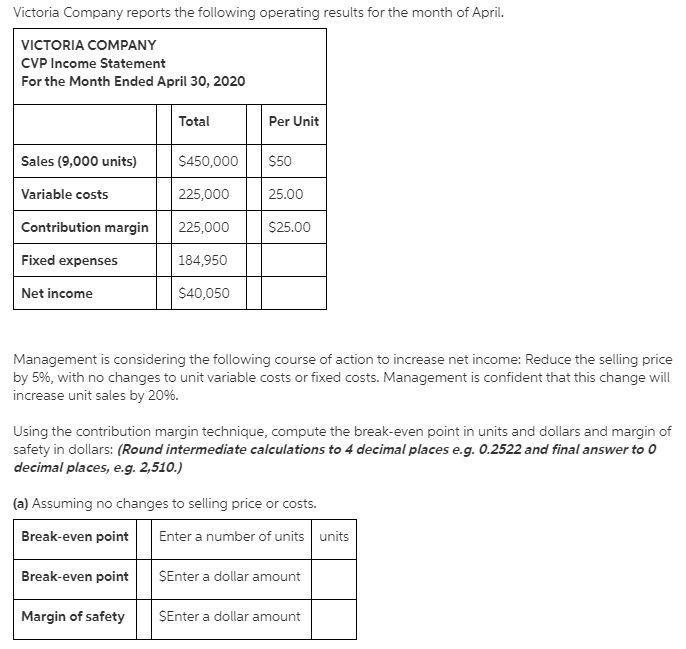

Answer:

Follows are the solution to the given question:

Explanation:

In this question, we assume that there is no change in selling price.

So,

False. indirect is not direct .