Answer: A

Explanation:

The one that is clearly out of place would be A

Community Supported Agriculture programs involve partnerships between food producers and local consumers in which the farms provide shares of their harvest with community members who support the farm by working on or financing the farm.

This partnership is important because it hedges the gap between the food producers and the local consumers who come together to provide food.

<h3>What is Partnership?</h3>

This refers to the arrangement where parties, known as business partners, agree to cooperate for a mutual benefit.

Hence, we can see that Community Supported Agriculture programs involve partnerships between food producers and local consumers in which the farms provide shares of their harvest with community members who support the farm by working on or financing the farm.

This partnership is important because it hedges the gap between the food producers and the local consumers who come together to provide food.

Read more about agric partnerships here:

brainly.com/question/24818860

#SPJ1

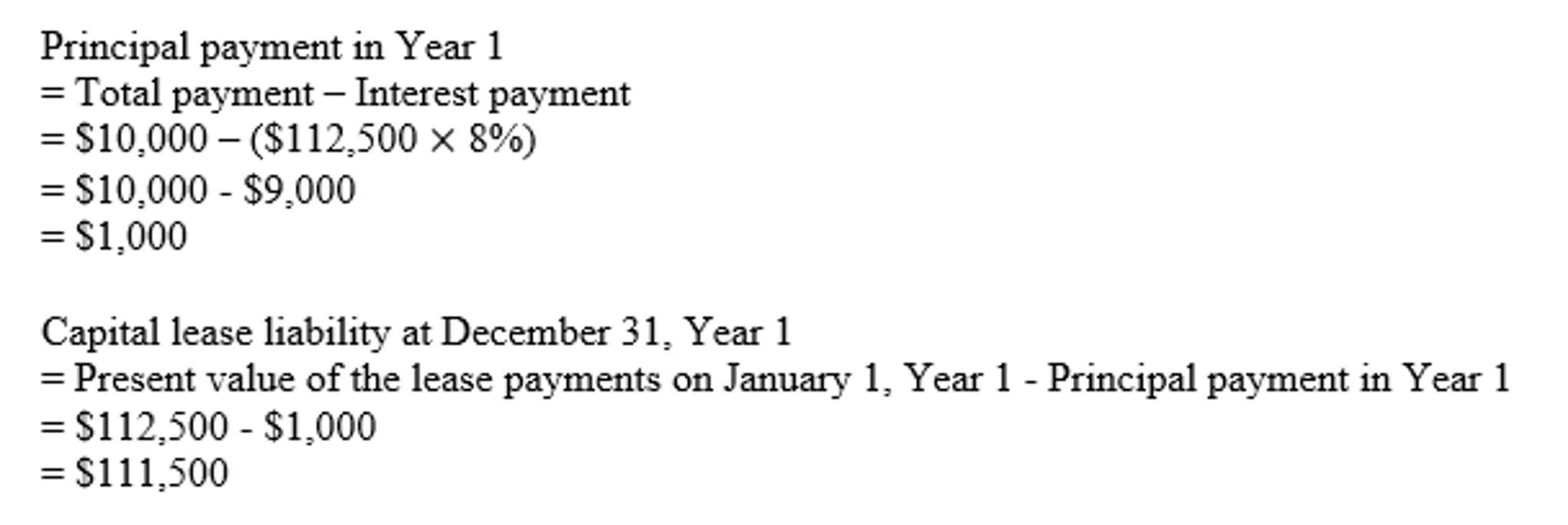

Answer

The answer and procedures of the exercise are attached in the following image.

Explanation

Please consider the data provided by the exercise. If you have any question please write me back. All the exercises are solved in a single sheet with the formulas indications.

Answer:

Supply chain management.

Explanation:

Supply chain management (SCM) is the structuring and coordination of relationships and activities across firms to deliver value in an information and technology intensive global environment.

Is the management of flows between and among supply chain stages to maximize total supply chain profitability.

All facilities, functions, activities, associated with flow and transformation of goods and services from raw materials to customer, as well as the associated information flow.

An intregated group of processes to source, make and deliver products.

Willing to pay for the stock today is $72.43.

Given values, Dividend = $1.85

Price = $80

return = 0.13

Formula, Current Price = (Dividend + Price ) / (1 + return )

= (1.85 + 80) / (1+ 0.13)

= $72.43

The number one purpose that buyers personal inventory is to earn a return on their funding. That go back commonly is available in viable methods: The stock's price appreciates, this means that it is going up. you can then promote the stock for a profit if you'd like.

The very best way to shop for stocks is thru a web stockbroker. After beginning and funding your account, you may buy shares via the broker's internet site in a remember of minutes. Other options encompass the use of a full-provider stockbroker, or shopping for inventory directly from the company.

Learn more about stock here:-

brainly.com/question/25818989

#SPJ4