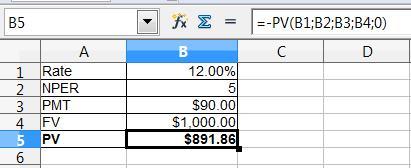

Answer:

$891.86

Explanation:

For this question, we use the Present value formula that is to be shown on the attachment. Kindly find it below:

Given that,

Future value = $1,000

Rate of interest = 12%

NPER = 5 years

PMT = $1,000 × 9% = $90

The formula is shown below:

= -PV(Rate;NPER;PMT;FV;type)

So, after solving this, the present value is $891.86

Answer:

The correct answer is option e.

Explanation:

Going to the concert will be a rational decision if the cost incurred is equal to the benefit earned.

Here, the ticket costs $50. Since the ticket is lost a new ticket is needed.

The value of time is $25.

The total cost will include both implicit as well as explicit costs.

The explicit cost is the cost of tickets. The implicit cost is the value of time.

The total cost involved is

= $50 + $50 + $25

= $125

For the decision to be rational the benefit earned should be at least equal to $125.

Answer:

b. Develop and present financial planning recommendations.

Explanation:

Since in the question it is mentioned that there is a recommendation for buying a personal liability with respect to the umbrella policy so in the steps of the financial planning process, the step that should be considered is to develop & present the recommendation with regard to the financial planning as the financial planning is important than can save your future

hence, the correct option is B.

I'm pretty sure it is d.

Hope this helps!