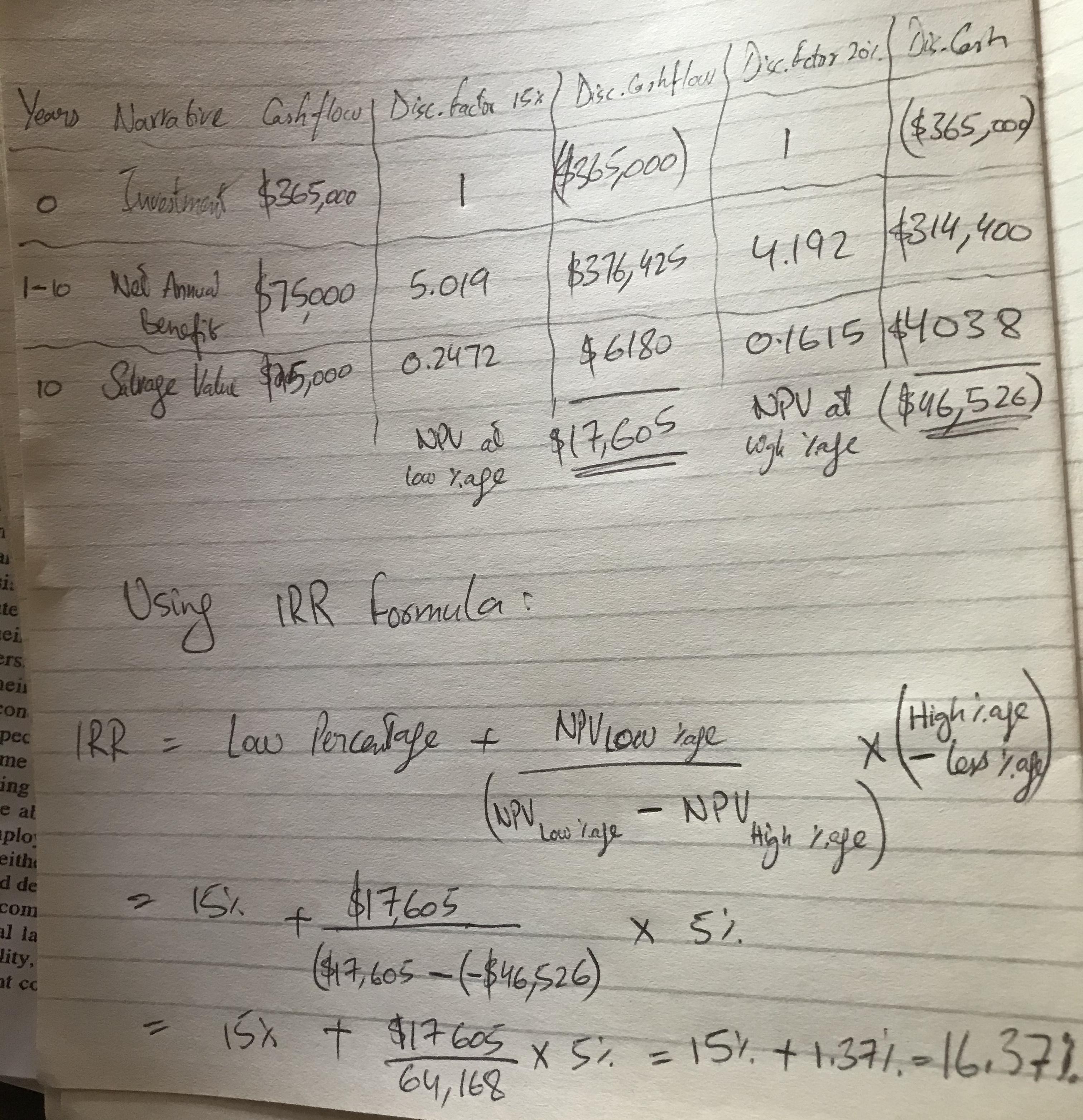

Answer:

The professor is wrong; the buyer should directly pay the car company at zero interest.

Explanation:

Lets first list down all the facts:

There are two options for the consumer - the first being pay directly cash to the car company at 0% interest or take a loan of the same amount. The discount is the same if the buyer manages to pay in time.

36 monthly payments implies 3 year period.

Use a spreadsheet to enter the above data and calculate the values. You have to calculate the NPV (net present value) of the investment in both the scenarios taking account of the rebate and the subsequant gain/loss in each option. Most spreadsheets use the NPV function, including Numbers for Mac.

Take the case for the first option, where interest is zero. These are the values that were found out:

For each year, cash flow is approx. $6,660 that makes upto $555.55 each month. This is the required payment the buyer needs to pay to the car company each year to be eligible for a discount.

In the end, the car will cost almost $18,000.

Now take the case for loan payment which has an interest of 5%.

As quite evident, the loan actually increases the pay burden, since the buyer has to pay the full $6,660 yearly to the car company in addition to paying interest to the bank which is almost $335 each year. So the total amount every year, to the buyer's account statement will be approx. $7000, a loss of more than $300 when compared to the previous situation.

In the end, the car will cost him more than $900 (almost $20,980), due to interest adding up every year. The dsicount of $2,000 will of course reduce the price of it, to like $18,980 but that is still $900 more than the zero interest offered by the car company.

Hence, according to my calculations, the professor is wrong; the buyer should directly pay the car company at zero interest.