Answer: hello your question is incomplete attached below is the complete question

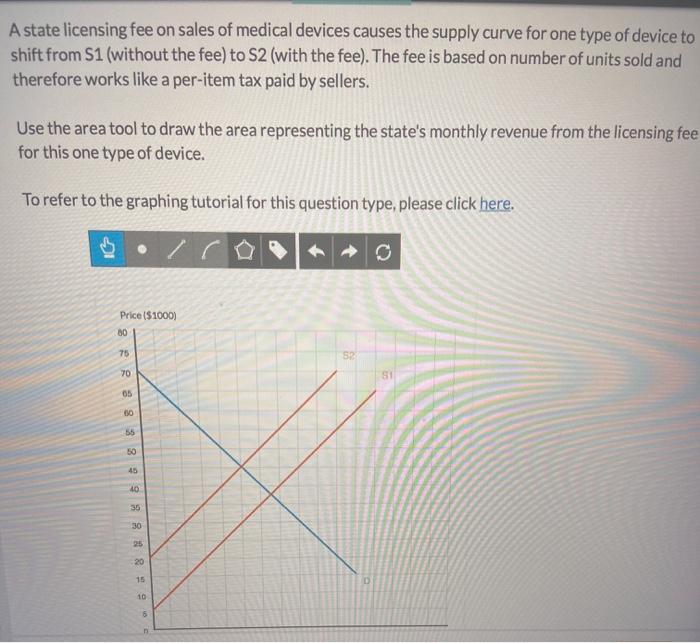

answer ; Government revenue from tax = $750,000 per month

Explanation:

Attached below is the required graph

Government revenue from tax ( per month )

= ( 450 - 30 ) ( 50 - 0 )

= $750,000 per month

Answer:

Option C is the correct answer.

<u>Debit Depletion Expense $1,358,500; credit Accumulated Depletion $1,358,500.</u>

Explanation:

Fortune Drilling Company acquires a mineral deposit at a cost of $5,900,000. It incurs additional costs of $600,000 to access the deposit, which is estimated to contain 2,000,000 tons and is expected to take 5 years to extract. Compute the depletion expense for the first year assuming 418,000 tons were mined.

Depletion expense = ( Mineral Deposit Cost + Additional cost)/ Estimate Extraction * N0 of ton extracted in first year

Depletion expense = (5900000 + 600000)/2000000 * 418000

Depletion expense = $ 1,358,500

Answer:

5th Nov is the latest date don could submit a event request.

Explanation:

- The marketing and sales event can both be organized at the health care. These events can be planned no less than 7 days of the colander before the day of the event. These event can e both formal and informal.

Answer:

Stories

Explanation:

Stories are the stuffs that the people hear about and like to discuss about. Stories are part of the organization culture and are a good means for an organization to affect customer choices because the issues of the customers are highlighted which helps organization to rectify its operations.

The correct answer is c

<span>c.measures the maximum amount the money supply can increase when new deposits enter the banking system

</span>

<span>. The money multiplier is the amount of money that banks generate with each dollar of reserves. Reserves is the amount of deposits that the Federal Reserve requires banks to hold and not lend. Banking reserves is the ratio of reserves to the total amount of deposits</span>