Answer:

decline.

Explanation:

The decline stage of the product's life cycle is marked by declining sales and product profitability. Generally, in this phase, the product begins to be replaced by new technologies, becomes outdated and goes into disuse.

It is important for companies to be aware that when entering this phase, the product needs redesign planning, so that improvements are implemented that make it updated to be relaunched in the market and then start another life cycle.

Opportunity cost refers to the alternative forgone.

Answer:

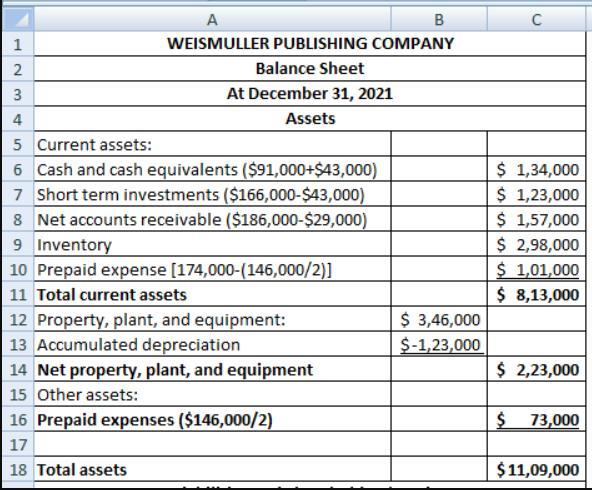

A balance sheet for Weismuller publishing for December 31 2021 was prepared and recorded in the explanation section below

Explanation:

Solution

COMPANY: WEISMULLER PUBLISHING Balance Sheet At December 31 2021 Assets

Current assets:

Cash and cash equivalents ($91,000 + $43000) $134000

Short term investments ($166,000 - $43000) $123000

The net accounts receivable ($186,000 =$29,000) $175,000

Inventory $298,000

Prepaid expense [174,000-(14600/2)] $101,000

The total current assets $813,000

Note: Kindly find an attached copy of the [art of the complete solution to this question below

Answer:

18.75%

Explanation:

Food Shoppe galore has a total market value stock of $650 million

The total market value of the company's debt is $150 million

The first step is to calculate the total market value of the company's capital

= $150,000,000 + $650,000,000

= $800,000,000

Therefore, the weighted average of the company's debt can be calculated as follows

= $150,000,000/$800,000,000

= 0.1875×100

= 18.75%

Hence the weighted average of the company's debt is 18.75%