It’s the value of the next best alternative when a decision is made, so not the first desired choice, but the second one

The Expenditure Approach adds up the market prices of final goods and services to calculate Gross Domestic Product (GDP)

The Expenditure Approach includes consumption expenditures, investments expenditures, government expenditures and net exports.

The Expenditure Approach is one of the 3 ways to measure economic production. The other 2 are The Production Approach and The Income Approach.

Answer:

ORGANIZATION EFFECTIVENESS IS MORE IMPORTANT THAN ORGANIZATIONAL PRODUCTIVITY.

Explanation:

Organizational productivity refers the skills of the company to produce the best results with the lowest costs. In this case the organization effectiveness refers to the skills that the company has to reach is objectives, hiking price increase organizational productivity, however in marketing terms it can be an obstacle to reach company objectives in the market reducing company effectiveness.

Answer:

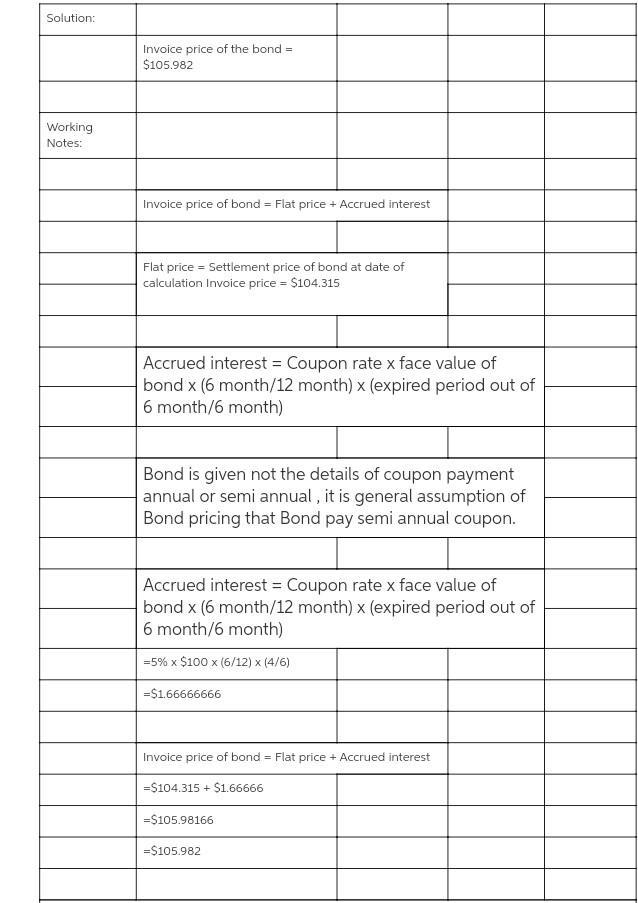

105.982

Explanation:

You should know before you proceed to the attached file for a step by step explanation of how the answer is gotten that, Bond is given, not the details of coupon payment, annual or semi annual, it is the general assumption of Bond pricing that bond pay semi annual coupon. Go through the attachment now for further explanation.

The type of consumer product that this represent is: Specialty product.

<h3>What is specialty product?</h3>

A specialty product is a consumer product that a person tend to buy or purchase because the product are specially made or because the buyer like the unique features of the product.

A consumer may choose to spend heavily on a product that are more expensive or tend to buy a particular products or brand because they like the product or because the product gives them what they want.

Inconclusion the type of consumer product that this represent is: Specialty product.

Learn more about specialty product here:brainly.com/question/7062667