The answer for the given statement above would be TRUE. What makes this true is that traffic patterns should be taken into consideration because this is the space in the room that people can walk through. Therefore, such furniture placements should be observed very well.

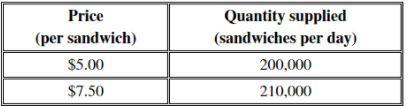

The daily price elasticity of supply is 0.1.

<h3>

What is the price elasticity of supply?</h3>

Price elasticity of supply measures the responsiveness of quantity supplied to changes in price of the good.

Price elasticity of supply = percentage change in quantity supplied / percentage change in price

Percentage change in quantity supplied = (210,000 / 200,000) - 1 = 5%

Percentage change in price = ($7.50 / $5) - 1 = 50%

Price elasticity of supply = 5%/50% = 0.1

Please find attached the required table. To learn more about price elasticity, please check: brainly.com/question/18850846

A or D

process of elimination..

B. (it’s verbal communication, not written)

C. (i highly doubt this is a possible answer.....but you are always willing to test that out for yourself)

E. (interpersonal is a conversation with oneself or “within a person”)

so now you’re left with A or D

C is the answer

Say thanks !

Answer:

The answer is option (d)$2.76

Explanation:

Solution

Given that:

The cost of a particular brand of toothpaste = 4 pounds

The exchange rate = .80

Real exchange rate = 1.16

Now

Real exchange rate is given as:

R = real exchange rate

e = nominal exchange rate

PF = foreign price

P = domestic price

Suppose we say that U.S. is a domestic country and British is a foreign country we have the following formula below:

R = e(PF/P)

R = 1.16

e = 0.80

PF = 4

Thus

R = e(PF/P)

1.16 = 0.80(4/P)

P = 3.2/1.16

= 2.7586207

= $2.76

Therefore, The U.S rice of the same toothpaste is about $2.76