Iron is the answer to the question

Answer:

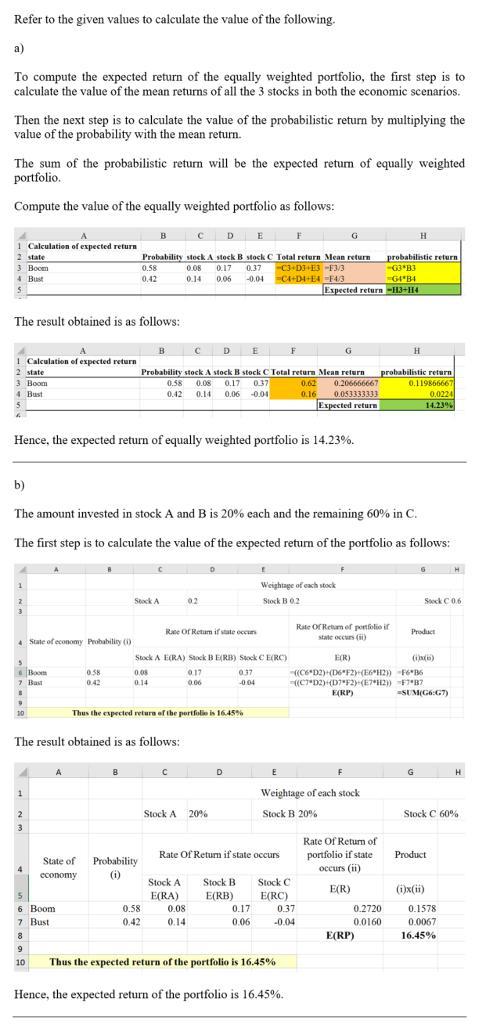

a) The expected return of equally weighed portfolio is 14.23%

b) The expected return of equally weighed portfolio is 16.45%, hence Variance = 1.596457%

Explanation:

See workings of a and b attached in a form of spreadsheet.

Answer:

intangible property

Explanation:

Intangible property can be defied as property that doesn't have any physical attributes that give them value. For example, a car is a tangible since you can drive it around, but a certificate of deposit is just a piece of paper (or even a computer code) and nothing else. The same applies to bonds and stocks, you know they are valuable but their value is not provided by their physical characteristics.

Other intangible property include patents, software, licenses, copyrights and trademarks. All of these can be extremely expensive, for example Microsoft is worth hundreds of billions and it sells digital ones and zeros.

Answer:

1. False

2. True

3. True

Explanation:

In Accounting, declaring and paying a stock dividend only decreases Retained Earnings but not Stockholders' Equity on the balance sheet because it has no effect on the cash position of an organization.

An inside director.

An inside director is someone who sits on the board of directors and is also an employee of the company (some board members are external non-employee advisors).