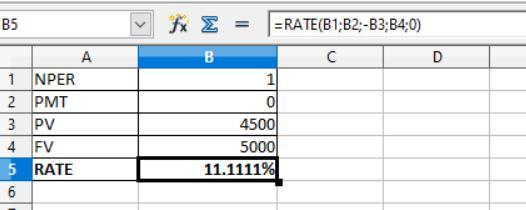

Answer:

11.11%

Explanation:

For computing the annual percentage rate (APR) we need to apply the RATE formula i.e to be shown in the attachment below.

Given that,

Present value = $5,000 × (100 - 10%) = $5,000 × 90% = $4,500

Future value or Face value = $5,000

PMT = 0

NPER = 1

The formula is shown below:

= -Rate(NPER;PMT;-PV;FV;type)

The present value come in negative

So, after applying the formula, the APR is 11.11%

Answer:

Th answer is: C) $13,000

Explanation:

The following amounts should be allocated to trust principal:

- $7,000 from the sale of bonds; those bonds were part of the trust principal

- $6,000 of stock dividends; new shares should be added to the trust principal since no cash was received

Earnings from rent ($1,000) and interest ($3,000) should be recorded as gross income.

Answer:

Significant noncash financing and investing activities.

Explanation:

Answer:

c. 0.9768

Explanation:

Lead time

Safety stock 500

Standard deviation 145

Safety stock = z * Standard deviation *

500 = z * 145*

500 = z * 251.14

Z = 1.990863

Therefore, for this Z value, we obtain the option c. 0.9768